What is chloropicrin, the chemical agent that Washington accuses Moscow of using in Ukraine?

What is chloropicrin, the chemical agent that Washington accuses Moscow of using in Ukraine? Poland, big winner of European enlargement

Poland, big winner of European enlargement In Israel, step-by-step negotiations for a ceasefire in the Gaza Strip

In Israel, step-by-step negotiations for a ceasefire in the Gaza Strip BBVA ADRs fall almost 2% on Wall Street

BBVA ADRs fall almost 2% on Wall Street Sánchez cancels his agenda and considers resigning: "I need to stop and reflect"

Sánchez cancels his agenda and considers resigning: "I need to stop and reflect" The Federal Committee of the PSOE interrupts the event to take to the streets with the militants

The Federal Committee of the PSOE interrupts the event to take to the streets with the militants Repsol: "We want to lead generative AI to guarantee its benefits and avoid risks"

Repsol: "We want to lead generative AI to guarantee its benefits and avoid risks" Osteoarthritis: an innovation to improve its management

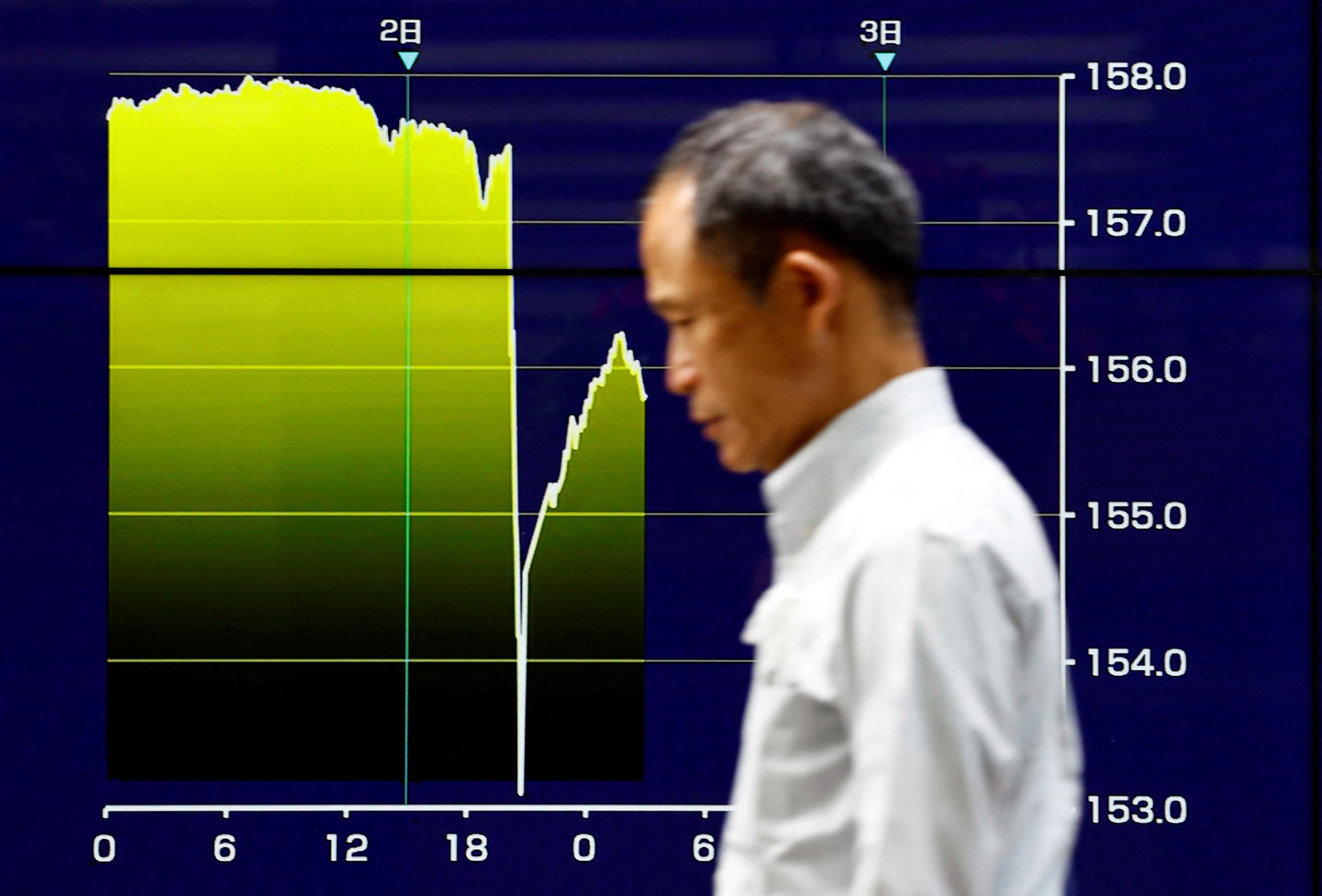

Osteoarthritis: an innovation to improve its management The yen jumps 3% then falls again, amid speculation of Japanese intervention

The yen jumps 3% then falls again, amid speculation of Japanese intervention A very busy Friday on the roads of Île-de-France before the Ascension Bridge

A very busy Friday on the roads of Île-de-France before the Ascension Bridge Fraud: the government is preparing new measures for the fall

Fraud: the government is preparing new measures for the fall Nike breaks the bank to keep the Blues jersey

Nike breaks the bank to keep the Blues jersey Madonna ends her world tour with a giant - and free - concert in Copacabana

Madonna ends her world tour with a giant - and free - concert in Copacabana Harry Potter: Daniel Radcliffe “really saddened” by his final breakup with J.K. Rowling

Harry Potter: Daniel Radcliffe “really saddened” by his final breakup with J.K. Rowling Leviathan, New York Trilogy... Five books by Paul Auster that you must have read

Leviathan, New York Trilogy... Five books by Paul Auster that you must have read Italy wins a decisive round against an American museum for the restitution of an ancient bronze

Italy wins a decisive round against an American museum for the restitution of an ancient bronze Omoda 7, another Chinese car that could be manufactured in Spain

Omoda 7, another Chinese car that could be manufactured in Spain BYD chooses CA Auto Bank as financial partner in Spain

BYD chooses CA Auto Bank as financial partner in Spain Tesla and Baidu sign key agreement to boost development of autonomous driving

Tesla and Baidu sign key agreement to boost development of autonomous driving Skoda Kodiaq 2024: a 'beast' plug-in hybrid SUV

Skoda Kodiaq 2024: a 'beast' plug-in hybrid SUV The home mortgage firm rises 3.8% in February and the average interest moderates to 3.33%

The home mortgage firm rises 3.8% in February and the average interest moderates to 3.33% This is how housing prices have changed in Spain in the last decade

This is how housing prices have changed in Spain in the last decade The home mortgage firm drops 10% in January and interest soars to 3.46%

The home mortgage firm drops 10% in January and interest soars to 3.46% The jewel of the Rocío de Nagüeles urbanization: a dream villa in Marbella

The jewel of the Rocío de Nagüeles urbanization: a dream villa in Marbella Europeans: a senior official on the National Rally list

Europeans: a senior official on the National Rally list Blockade of Sciences Po: the right denounces a “drift”, the government charges the rebels

Blockade of Sciences Po: the right denounces a “drift”, the government charges the rebels Even on a mission for NATO, the Charles-de-Gaulle remains under French control, Lecornu responds to Mélenchon

Even on a mission for NATO, the Charles-de-Gaulle remains under French control, Lecornu responds to Mélenchon “Deadly Europe”, “economic decline”, immigration… What to remember from Emmanuel Macron’s speech at the Sorbonne

“Deadly Europe”, “economic decline”, immigration… What to remember from Emmanuel Macron’s speech at the Sorbonne These French cities that will boycott the World Cup in Qatar

These French cities that will boycott the World Cup in Qatar Mercato: Verratti at Barça? A track studied

Mercato: Verratti at Barça? A track studied Rugby: after the defeat during the Six Nations, the Blues will meet the English in September for a test match

Rugby: after the defeat during the Six Nations, the Blues will meet the English in September for a test match Premier League: Liverpool unveils its new jersey for next season

Premier League: Liverpool unveils its new jersey for next season Formula 1: Alpine holds its new executive technical director

Formula 1: Alpine holds its new executive technical director

In recent months, the Euribor's rise has cooled the fury of the mortgage company. It is true that the triggered inflation has reduced the economy. The level of 2019 will not be regained until 2024.

Despite the current economic situation, many people take out mortgages from banks to afford a home. The Organization of Consumers and Users has issued a notice to this effect that is sure to be of interest to many.

Can a bank require people to get home or life insurance if they take out a mortgage? The law permits entities to require the hire of an insurance policy in order to guarantee the loan repayment or to protect the guarantee.

As the OCU affirms they can't impose their insurance, it begs the question: As long as coverage is maintained, the consumer can choose the company with which he contracts.

The bank may discount the interest rate on their mortgages by referring to additional products. Contracting is not required in this instance. However, a series reductions in the interest rate will be applied to those who decide to contract these products. According to OCU, the closer the relationship, the better conditions are offered.

It is important to calculate if the insurance is worth the cost of the bank company's insurance, which is almost always more expensive in exchange for a lower mortgage differential.

The bank may require that you contract insurance in order to grant the loan. This must be stated in the deed. It will not be possible for you to cancel the contract while the loan remains in force as indicated by OCU's website.

The client cannot cancel compulsory contracting products or pay the premium. The entity also reserves the right not to contract the insurance premium and to pass the cost on to the client. You can change insurance to another company as long as the coverage is the same.

If the bonus was for the mortgage to contract a particular insurance with a company, cancelling that insurance or changing the company will mean you are not meeting the interest rate requirements.

Insurers often inform clients of the premiums that they will be paying after each renewal. The regulations don't require that this information be provided. Therefore, the only obligation an insurer has to inform the client about the new annual premium at the least two months prior to each annuity's expiration is to notify them of the change.

In most cases, the premium paid for the mortgage and insurance will not be reported.

OCU recommends that you review each year to determine if the insurance is still worth your time or whether it is more convenient to cancel the policy or change insurance companies. It all depends on the premium. Cancelling or changing insurance companies can be fun, even if you lose the bonus.