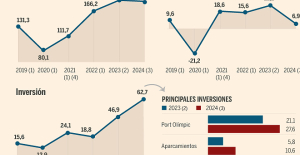

B:SM will break its investment record this year with 62 million euros

B:SM will break its investment record this year with 62 million euros War in Ukraine: when kyiv attacks Russia with inflatable balloons loaded with explosives

War in Ukraine: when kyiv attacks Russia with inflatable balloons loaded with explosives United States: divided on the question of presidential immunity, the Supreme Court offers respite to Trump

United States: divided on the question of presidential immunity, the Supreme Court offers respite to Trump Maurizio Molinari: “the Scurati affair, a European injury”

Maurizio Molinari: “the Scurati affair, a European injury” First three cases of “native” cholera confirmed in Mayotte

First three cases of “native” cholera confirmed in Mayotte Meningitis: compulsory vaccination for babies will be extended in 2025

Meningitis: compulsory vaccination for babies will be extended in 2025 Spain is the country in the European Union with the most overqualified workers for their jobs

Spain is the country in the European Union with the most overqualified workers for their jobs Parvovirus alert, the “fifth disease” of children which has already caused the death of five babies in 2024

Parvovirus alert, the “fifth disease” of children which has already caused the death of five babies in 2024 Inflation rebounds in March in the United States, a few days before the Fed meeting

Inflation rebounds in March in the United States, a few days before the Fed meeting Video games: Blizzard cancels Blizzcon 2024, its annual high mass

Video games: Blizzard cancels Blizzcon 2024, its annual high mass Falling wings of the Moulin Rouge: who will pay for the repairs?

Falling wings of the Moulin Rouge: who will pay for the repairs? “You don’t sell a company like that”: Roland Lescure “annoyed” by the prospect of a sale of Biogaran

“You don’t sell a company like that”: Roland Lescure “annoyed” by the prospect of a sale of Biogaran Exhibition: in Deauville, Zao Wou-Ki, beauty in all things

Exhibition: in Deauville, Zao Wou-Ki, beauty in all things Dak’art, the most important biennial of African art, postponed due to lack of funding

Dak’art, the most important biennial of African art, postponed due to lack of funding In Deadpool and Wolverine, Ryan and Hugh Jackman explore the depths of the Marvel multiverse

In Deadpool and Wolverine, Ryan and Hugh Jackman explore the depths of the Marvel multiverse Tom Cruise returns to Paris for the filming of Mission Impossible 8

Tom Cruise returns to Paris for the filming of Mission Impossible 8 Skoda Kodiaq 2024: a 'beast' plug-in hybrid SUV

Skoda Kodiaq 2024: a 'beast' plug-in hybrid SUV Tesla launches a new Model Y with 600 km of autonomy at a "more accessible price"

Tesla launches a new Model Y with 600 km of autonomy at a "more accessible price" The 10 best-selling cars in March 2024 in Spain: sales fall due to Easter

The 10 best-selling cars in March 2024 in Spain: sales fall due to Easter A private jet company buys more than 100 flying cars

A private jet company buys more than 100 flying cars This is how housing prices have changed in Spain in the last decade

This is how housing prices have changed in Spain in the last decade The home mortgage firm drops 10% in January and interest soars to 3.46%

The home mortgage firm drops 10% in January and interest soars to 3.46% The jewel of the Rocío de Nagüeles urbanization: a dream villa in Marbella

The jewel of the Rocío de Nagüeles urbanization: a dream villa in Marbella Rental prices grow by 7.3% in February: where does it go up and where does it go down?

Rental prices grow by 7.3% in February: where does it go up and where does it go down? Even on a mission for NATO, the Charles-de-Gaulle remains under French control, Lecornu responds to Mélenchon

Even on a mission for NATO, the Charles-de-Gaulle remains under French control, Lecornu responds to Mélenchon “Deadly Europe”, “economic decline”, immigration… What to remember from Emmanuel Macron’s speech at the Sorbonne

“Deadly Europe”, “economic decline”, immigration… What to remember from Emmanuel Macron’s speech at the Sorbonne Sale of Biogaran: The Republicans write to Emmanuel Macron

Sale of Biogaran: The Republicans write to Emmanuel Macron Europeans: “All those who claim that we don’t need Europe are liars”, criticizes Bayrou

Europeans: “All those who claim that we don’t need Europe are liars”, criticizes Bayrou These French cities that will boycott the World Cup in Qatar

These French cities that will boycott the World Cup in Qatar Euroleague: at the end of the suspense, Monaco equalizes against Fenerbahçe

Euroleague: at the end of the suspense, Monaco equalizes against Fenerbahçe Women's Six Nations: Where to see and five things to know about France-England

Women's Six Nations: Where to see and five things to know about France-England Liverpool: it is confirmed, Slot will succeed Klopp on the Reds bench

Liverpool: it is confirmed, Slot will succeed Klopp on the Reds bench Ligue 1: Montpellier and Nantes back to back, two reds in stoppage time

Ligue 1: Montpellier and Nantes back to back, two reds in stoppage time

The euro zone economy moves closer to stabilization in February thanks to the services sector, which achieved slight growth: the HCOB PMI Composite Index of total activity stood at 49.2 points (47.9 in January), highs in the last eight months , and the PMI subindex of commercial activity in the services sector stood at 50.2 (48.4 in January), marking its highest level in seven months.

The PMI, the main indicator of the private economy that precedes the evolution of the GDP, remained in contraction territory, below 50 points but is at a level close to stabilization for the euro zone economy. But a new contraction in the manufacturing sector neutralizes this renewed expansion in the service sector. "It is evident that the services sector is reviving, but the slowdown in the manufacturing sector continued to offset this growth," says the report published today by S

"Despite total activity volumes falling for the ninth consecutive month, the contraction was marginal and the slowest since mid-2023. Services companies recorded a slight improvement in commercial activity, which was offset by a further solid reduction in manufacturing production.

"The slowdown in demand, one of the main factors responsible for the euro zone's economic decline since mid-2023, also eased for the fourth consecutive month, helping to boost growth expectations to their highest in almost twelve months and revitalize the employment creation".

However, amid reports of persistent wage pressures, overall operating costs rose by the most in ten months, causing a further rise in price inflation.

There were notable differences in the economic performance of the countries included in the Eurozone PMI. Solid expansions were seen in Ireland and Spain.

Business activity in the private sector in Ireland increased at a solid pace, which was the fastest in the last twelve months, while the pace of growth in Spain improved to a nine-month high. Italy also made a positive contribution, although its expansion was modest.

However, this growth was offset by the two main economies of the euro zone, France and Germany, which remain immersed in a contraction. While France's economic slowdown eased, Germany's decline accelerated to its fastest pace since October 2023.

The biggest drag on economic activity in the euro in general continued to be that of export markets, especially among companies in the manufacturing sector continued to drive the reduction. However, job creation recovered in the middle of the first quarter: the employment growth rate, although modest, was a seven-month high in the fifth consecutive monthly improvement in business optimism, especially in services.

Regarding price trends, February survey data pointed to intensifying pressures across the eurozone. Input costs continued to rise and the inflation rate accelerated to a ten-month high. "Costs borne by the service sector were responsible, although manufacturing sector costs fell at a weaker rate than at the beginning of the year. In turn, prices charged for euro zone products and services rose at the same rate fastest since May 2023."

"As has been the case over the past three years, inflationary pressures in the services sector were high. Although not as severe as that observed between 2021 and 2023, the rate of increase rose to its highest in nine months and was very "above their long-term average. Likewise, prices charged increased at a marked and accelerated pace."

Cyrus de la Rubia, chief economist at Hamburg Commercial Bank, points out that "it is possible that the services sector has started 2024 better than expected (...). In fact, the stability of new orders suggests the probability of a turning point. inflection in demand conditions".

"The economic vitality of the euro zone's services sector predominantly originated in the south: Spain and Italy marked their sixth and second consecutive months of increases in service sector business activity respectively, in contrast to Germany and France."

However, "the four main euro zone economies have in common a robust pace of employee hiring. Although employment is traditionally considered a lagging indicator, this trend points to a growing sense of optimism and suggests that the recovery of the sector will continue," he continues in a commentary accompanying the report.

"As the European Central Bank (ECB) prepares for its meeting on March 7, attention is focused on heated discussions over the appropriate time to cut interest rates."

In this regard, the PMI survey provides two important contributions. "First, prices charged by the services sector continue to rise at a rapid pace, driven primarily by rising wage costs. Second, the unexpectedly robust pricing power demonstrated by service companies amid a climate sluggish economy and the forecast of growth below 1% for 2024 arouses astonishment".

"This intensifies concerns about the possible emergence of a wage-price spiral and stagflation, especially given persistent structural labor shortages that threaten productivity. The PMI findings may support those who recommend cutting interest rates later."