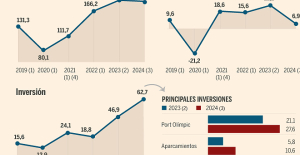

B:SM will break its investment record this year with 62 million euros

B:SM will break its investment record this year with 62 million euros War in Ukraine: when kyiv attacks Russia with inflatable balloons loaded with explosives

War in Ukraine: when kyiv attacks Russia with inflatable balloons loaded with explosives United States: divided on the question of presidential immunity, the Supreme Court offers respite to Trump

United States: divided on the question of presidential immunity, the Supreme Court offers respite to Trump Maurizio Molinari: “the Scurati affair, a European injury”

Maurizio Molinari: “the Scurati affair, a European injury” First three cases of “native” cholera confirmed in Mayotte

First three cases of “native” cholera confirmed in Mayotte Meningitis: compulsory vaccination for babies will be extended in 2025

Meningitis: compulsory vaccination for babies will be extended in 2025 Spain is the country in the European Union with the most overqualified workers for their jobs

Spain is the country in the European Union with the most overqualified workers for their jobs Parvovirus alert, the “fifth disease” of children which has already caused the death of five babies in 2024

Parvovirus alert, the “fifth disease” of children which has already caused the death of five babies in 2024 Inflation rebounds in March in the United States, a few days before the Fed meeting

Inflation rebounds in March in the United States, a few days before the Fed meeting Video games: Blizzard cancels Blizzcon 2024, its annual high mass

Video games: Blizzard cancels Blizzcon 2024, its annual high mass Falling wings of the Moulin Rouge: who will pay for the repairs?

Falling wings of the Moulin Rouge: who will pay for the repairs? “You don’t sell a company like that”: Roland Lescure “annoyed” by the prospect of a sale of Biogaran

“You don’t sell a company like that”: Roland Lescure “annoyed” by the prospect of a sale of Biogaran Exhibition: in Deauville, Zao Wou-Ki, beauty in all things

Exhibition: in Deauville, Zao Wou-Ki, beauty in all things Dak’art, the most important biennial of African art, postponed due to lack of funding

Dak’art, the most important biennial of African art, postponed due to lack of funding In Deadpool and Wolverine, Ryan and Hugh Jackman explore the depths of the Marvel multiverse

In Deadpool and Wolverine, Ryan and Hugh Jackman explore the depths of the Marvel multiverse Tom Cruise returns to Paris for the filming of Mission Impossible 8

Tom Cruise returns to Paris for the filming of Mission Impossible 8 Skoda Kodiaq 2024: a 'beast' plug-in hybrid SUV

Skoda Kodiaq 2024: a 'beast' plug-in hybrid SUV Tesla launches a new Model Y with 600 km of autonomy at a "more accessible price"

Tesla launches a new Model Y with 600 km of autonomy at a "more accessible price" The 10 best-selling cars in March 2024 in Spain: sales fall due to Easter

The 10 best-selling cars in March 2024 in Spain: sales fall due to Easter A private jet company buys more than 100 flying cars

A private jet company buys more than 100 flying cars This is how housing prices have changed in Spain in the last decade

This is how housing prices have changed in Spain in the last decade The home mortgage firm drops 10% in January and interest soars to 3.46%

The home mortgage firm drops 10% in January and interest soars to 3.46% The jewel of the Rocío de Nagüeles urbanization: a dream villa in Marbella

The jewel of the Rocío de Nagüeles urbanization: a dream villa in Marbella Rental prices grow by 7.3% in February: where does it go up and where does it go down?

Rental prices grow by 7.3% in February: where does it go up and where does it go down? Even on a mission for NATO, the Charles-de-Gaulle remains under French control, Lecornu responds to Mélenchon

Even on a mission for NATO, the Charles-de-Gaulle remains under French control, Lecornu responds to Mélenchon “Deadly Europe”, “economic decline”, immigration… What to remember from Emmanuel Macron’s speech at the Sorbonne

“Deadly Europe”, “economic decline”, immigration… What to remember from Emmanuel Macron’s speech at the Sorbonne Sale of Biogaran: The Republicans write to Emmanuel Macron

Sale of Biogaran: The Republicans write to Emmanuel Macron Europeans: “All those who claim that we don’t need Europe are liars”, criticizes Bayrou

Europeans: “All those who claim that we don’t need Europe are liars”, criticizes Bayrou These French cities that will boycott the World Cup in Qatar

These French cities that will boycott the World Cup in Qatar Euroleague: at the end of the suspense, Monaco equalizes against Fenerbahçe

Euroleague: at the end of the suspense, Monaco equalizes against Fenerbahçe Women's Six Nations: Where to see and five things to know about France-England

Women's Six Nations: Where to see and five things to know about France-England Liverpool: it is confirmed, Slot will succeed Klopp on the Reds bench

Liverpool: it is confirmed, Slot will succeed Klopp on the Reds bench Ligue 1: Montpellier and Nantes back to back, two reds in stoppage time

Ligue 1: Montpellier and Nantes back to back, two reds in stoppage time

At the conclusion of the supplementary insurance is offered to attention. On the one hand, you have to be to the individual needs of the Insured fairly, on the other hand, over-insurance can go a pretty penny. Because the basic health insurance policy in addition to voluntary additional benefits are many and varied. With the highest cost of the additional Hospital in which the Insured to choose whether they want to be treated in a private or semi-private ward is connected.

1. Supplementary insurance only after recording in new Fund

Who buy supplemental insurance or an Upgrade from semi-private to private would like to make, is dismissed by many health insurance companies of a certain age or in a worse state of health terminate. It is therefore particularly important to terminate the existing policy only if it has the written commitment of the recording in any other Fund is available.

semi-private or private insurance coverage? Financially, a giant makes this difference. Photo: Andre Muelhaupt

2. Health Declaration truthfully

fill out The supplementary hospital insurance covers an important need. The amount of the insurance contributions depends on the scope of work, age and health of the Insured. Depending on the insurance company's customers can no longer switch from the fifty or sixty years, the hospital auxiliary, but only fold or deeper insurance coverage to choose. In the case of an exchange, often a health Declaration must be supplied. These must be truthfully filled in, in order to prevent a subsequent exclusion from the health insurance Fund.

3. In the case of hospital insurance, Flex-model

The stay in the General ward choose is covered by the basic insurance. Many Insured a semi-private or private insurance coverage, however, is too expensive for you, the flexible hospital insurance (Flex model) is suitable. Prior to the hospital admission is selected, which Department, respectively, of treatment is desired. The Insured decides for semi-private or private, must contribute to the cost. His current premiums are significantly lower. In addition, this Cost sharing may be covered by means of a daily hospital allowance insurance.

4. Exclude accident cover

employees with a workload of more than eight hours per week are not for the same employer in the case of occupational and non - occupational accidents on the insurance of the employer are covered. In contrast, the accident cover may be excluded in the additional insurance but never. They is usually cheap, and their subsequent inclusion may be subject to limitations.

5. In the case of scheduled maternity leave period to clarify

to be able to during pregnancy and at birth over and above the basic insurance in addition to benefits, it must be ensured that they do not fall in any waiting period. Women planning a maternity, should promptly clarify, when what services are covered.

6. Children before birth to insure

children must be insured before birth. This is free of charge, guarantees, however, that the child may be a birth defects unconditionally in the supplementary insurance included.

Even with the dental insurance for the children, money can be saved. Photo: LAB

7. Dental insurance for the birth of the child to complete

don't be surprised To parents later of high claims, you should sign up for the birth of the child, or before his sixth birthday, a dental insurance, the basic insurance pays nothing on dental corrections. Many insurers require from the sixth birthday of a dentist's certificate; in the case of a misalignment of the teeth position, the cover can no longer be completed. It is therefore recommended that at birth a dental insurance with a high insurance protection.

8. Lump-sum disability benefit for children and Housewives

The 2 insure. Pillar provides for the Insured a lump-sum Disability benefit in case of disability. Children, Housewives, and students are not insured against the financial consequences of this, in the worst Case, however, sufficient, since no appropriate cover from the 2. Pillar is. It must therefore be concluded for sure a suitable insurance for disability due to illness or accident.

9. Call dates

When there is a change or adaptation of additional insurance to comply with certain deadlines must be observed. In the case of a premium increase about the additional insurance can be changed until the end of November, the notice must be received by no later than the last working day in November for health insurance.

10. Additional insurance on time complete

It is possible already now additional insurance by 1. January 2021 to complete. The basic insurance can be changed at the beginning of 2020 to a new insurer – and a year later, the additional insurance companies come to.

Stephan Wirz, member of the management Board of the broker centre of Switzerland AG

This Text comes from the leaflet "money & Digital" in the current issue. Now all of the articles in the E-Paper of the Sunday newspaper, read: App for iOS App for Android – Web-App

Created: 15.11.2019, 11:09 PM