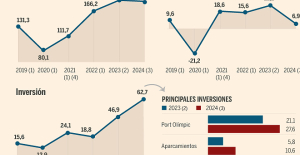

B:SM will break its investment record this year with 62 million euros

B:SM will break its investment record this year with 62 million euros War in Ukraine: when kyiv attacks Russia with inflatable balloons loaded with explosives

War in Ukraine: when kyiv attacks Russia with inflatable balloons loaded with explosives United States: divided on the question of presidential immunity, the Supreme Court offers respite to Trump

United States: divided on the question of presidential immunity, the Supreme Court offers respite to Trump Maurizio Molinari: “the Scurati affair, a European injury”

Maurizio Molinari: “the Scurati affair, a European injury” First three cases of “native” cholera confirmed in Mayotte

First three cases of “native” cholera confirmed in Mayotte Meningitis: compulsory vaccination for babies will be extended in 2025

Meningitis: compulsory vaccination for babies will be extended in 2025 Spain is the country in the European Union with the most overqualified workers for their jobs

Spain is the country in the European Union with the most overqualified workers for their jobs Parvovirus alert, the “fifth disease” of children which has already caused the death of five babies in 2024

Parvovirus alert, the “fifth disease” of children which has already caused the death of five babies in 2024 Inflation rebounds in March in the United States, a few days before the Fed meeting

Inflation rebounds in March in the United States, a few days before the Fed meeting Video games: Blizzard cancels Blizzcon 2024, its annual high mass

Video games: Blizzard cancels Blizzcon 2024, its annual high mass Falling wings of the Moulin Rouge: who will pay for the repairs?

Falling wings of the Moulin Rouge: who will pay for the repairs? “You don’t sell a company like that”: Roland Lescure “annoyed” by the prospect of a sale of Biogaran

“You don’t sell a company like that”: Roland Lescure “annoyed” by the prospect of a sale of Biogaran Exhibition: in Deauville, Zao Wou-Ki, beauty in all things

Exhibition: in Deauville, Zao Wou-Ki, beauty in all things Dak’art, the most important biennial of African art, postponed due to lack of funding

Dak’art, the most important biennial of African art, postponed due to lack of funding In Deadpool and Wolverine, Ryan and Hugh Jackman explore the depths of the Marvel multiverse

In Deadpool and Wolverine, Ryan and Hugh Jackman explore the depths of the Marvel multiverse Tom Cruise returns to Paris for the filming of Mission Impossible 8

Tom Cruise returns to Paris for the filming of Mission Impossible 8 Skoda Kodiaq 2024: a 'beast' plug-in hybrid SUV

Skoda Kodiaq 2024: a 'beast' plug-in hybrid SUV Tesla launches a new Model Y with 600 km of autonomy at a "more accessible price"

Tesla launches a new Model Y with 600 km of autonomy at a "more accessible price" The 10 best-selling cars in March 2024 in Spain: sales fall due to Easter

The 10 best-selling cars in March 2024 in Spain: sales fall due to Easter A private jet company buys more than 100 flying cars

A private jet company buys more than 100 flying cars This is how housing prices have changed in Spain in the last decade

This is how housing prices have changed in Spain in the last decade The home mortgage firm drops 10% in January and interest soars to 3.46%

The home mortgage firm drops 10% in January and interest soars to 3.46% The jewel of the Rocío de Nagüeles urbanization: a dream villa in Marbella

The jewel of the Rocío de Nagüeles urbanization: a dream villa in Marbella Rental prices grow by 7.3% in February: where does it go up and where does it go down?

Rental prices grow by 7.3% in February: where does it go up and where does it go down? Even on a mission for NATO, the Charles-de-Gaulle remains under French control, Lecornu responds to Mélenchon

Even on a mission for NATO, the Charles-de-Gaulle remains under French control, Lecornu responds to Mélenchon “Deadly Europe”, “economic decline”, immigration… What to remember from Emmanuel Macron’s speech at the Sorbonne

“Deadly Europe”, “economic decline”, immigration… What to remember from Emmanuel Macron’s speech at the Sorbonne Sale of Biogaran: The Republicans write to Emmanuel Macron

Sale of Biogaran: The Republicans write to Emmanuel Macron Europeans: “All those who claim that we don’t need Europe are liars”, criticizes Bayrou

Europeans: “All those who claim that we don’t need Europe are liars”, criticizes Bayrou These French cities that will boycott the World Cup in Qatar

These French cities that will boycott the World Cup in Qatar Euroleague: at the end of the suspense, Monaco equalizes against Fenerbahçe

Euroleague: at the end of the suspense, Monaco equalizes against Fenerbahçe Women's Six Nations: Where to see and five things to know about France-England

Women's Six Nations: Where to see and five things to know about France-England Liverpool: it is confirmed, Slot will succeed Klopp on the Reds bench

Liverpool: it is confirmed, Slot will succeed Klopp on the Reds bench Ligue 1: Montpellier and Nantes back to back, two reds in stoppage time

Ligue 1: Montpellier and Nantes back to back, two reds in stoppage time

The current Swedish tax system is in great need of a comprehensive tax reform. Therefore, the driver Timbro a skattereformsprojekt which presents the proposal for a tax system that is simpler, characterized by uniformity and have lower tax rates. On kapitalskatternas area, we have proposed halving the corporate tax lowered kapitalinkomstskatt to 15 per cent. When it comes to taxes on work, we have proposed a personal allowance for earned income in 10,000 sek per month and the elimination of the state income tax.

today we release a new report, which deals with tax on consumption, i.e. vat. Vat stands for almost every fourth skattekrona, with close to 500 billion in revenue. It affects a large number of decisions by households, companies and municipalities. Nonetheless, it is not at all in the Januariöverenskommelsen.

the Inspiration comes from New Zealand, which has a modern vat system with a broad tax base and uniform tax rate.

Inspiration comes from New Zealand, which has a modern vat system with a broad tax base and uniform tax rate.

1 Facing the uniform vat rate. The various rates 6, 12 and 25 per cent creates boundary problems and economic losses when the tax system interferes with the price signal. In addition, it is unfair to anyone who buys a lot of food or travel very taxi pay less vat than others. The national audit office recently confirmed that the reduction of matmomsen not a fördelningspolitiskt accurate measure, something that government investigations have pointed out for decades.

If the vat was set at 21.3 per cent, would the reform be revenue neutral. A general increase to 25 percent would raise 63 billion, which can be used for other tax cuts, such as on labor and capital.

2 Broaden the tax base for vat. One-third of the private consumption is exempt from vat. It creates problems because companies that are not subject to the tax may not deduct vat on their purchases. Thus, they have incentives to use their own personnel in the business rather than to outsource or to invest in machinery. It counteracts efficiency. In addition, provides for exemptions from vat rise to a lot of administrative costs, especially for businesses engaged in both taxable and exempt activities or changing the tax status.

residential rentals is one of the areas covered by the vat exemption. It creates a lot of hassle, especially for companies that also rent out the premises or that want to convert the premises to residential or vice versa. Rents should therefore momsbeläggas. The question is what tax rate should be chosen. The property owners, the tenants ' association and Sabo advocates a 6-percent vat on rents, property companies should be able to deduct the input vat.

For likformighetens sake, however, should housing be taxed in the same way as other consumption. It need not involve a sharp tax increase. According to our calculations, a 25% vat on the rents to reduce tax revenue by sek 7 billion in the short term, as vat on investments would become tax deductible.

Gaming companies are exempt, but it is an industry that is fully possible to momsbelägga, which there are several international examples. Banking and insurance services are not covered by the vat, which historically has been motivated by practical difficulties. New Zealand shows, however, that it is possible to momsbelägga property and casualty insurance. Sweden can't make it on your own, but it requires changes in the EU vat directive. Two other exceptions that should be addressed at EU-level is a postal service and international passenger transport.

With the help of previously unpublished statistics from Statistics sweden, we can calculate how finances would be affected by a broader tax base for vat. If, in principle, all private consumption were taxed, would the tax base to increase by 330 billion, which corresponds to 65 billion in tax revenue. At the same time, industries that will be vat get deduct vat on their purchases, equivalent to 52 billion. The net increase of tax revenue would be 13 billion, which can be used for other tax reductions.

the main point of the reform is, however, not to increase tax revenue, without creating greater uniformity and to reduce the damage to the national economy.

3 Add the vat in the public sector. The public sector remains outside the EU's vat system, as well as education, health and social care, as they have traditionally been provided by the public. There are good reasons to add vat also on public businesses, such as New Zealand do. One reason is that local government's zero vat makes the local consumption becomes relatively cheaper than private consumption. It can put upward pressure on kommunalskatterna.

this vat exemption also means that the private välfärdsföretagen not allowed to deduct vat on their purchases, expensive outsourcing and the purchase of medical equipment. The problem is compounded by a recent judgment of the Supreme administrative court, which established that the hiring of healthcare workers are liable.

Therefore, it requires courage from the politicians to resist vested interests and to ensure the public interest. A modern tax system promotes effort and entrepreneurship with generally low tax rates, not by targeted tax breaks to certain industries.

the tax reform, as promised in the januariöverenskommelsen is an excellent opportunity to implement a restructuring of the vat, as you then can implement multiple changes at the same time. Then the losers in a certain extent be compensated and vested interests is more difficult to mobilise in order to stop the reform.

The parties participating in the upcoming tax reform should also implement a tax shift from taxes on labour and capital to the vat, in the context of an overall reduced tax burden. This is because a well designed tax is one of the very best ways to finance government expenditure. Vat taxes consumption and therefore reduces not incentives to save and invest. In addition, it has built-in mechanisms that hinder tax evasion.

Despite the fact that the EUROPEAN commission engaged in a work to reform the vat directive, some years ago the changes announced too small and too focused on the fight against tax evasion rather than to reduce the regulatory burden and improving growth.

Reform efforts encounter on patrol here, too. One example is the Swedish association of local authorities and regions, SALAR, as opposed to the municipalities to be incorporated in the vat system. The Swedish government should take a leading position in this debate, within the EU and not be hampered by special interests.