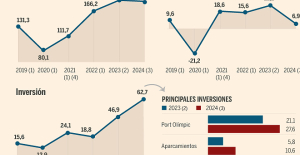

B:SM will break its investment record this year with 62 million euros

B:SM will break its investment record this year with 62 million euros War in Ukraine: when kyiv attacks Russia with inflatable balloons loaded with explosives

War in Ukraine: when kyiv attacks Russia with inflatable balloons loaded with explosives United States: divided on the question of presidential immunity, the Supreme Court offers respite to Trump

United States: divided on the question of presidential immunity, the Supreme Court offers respite to Trump Maurizio Molinari: “the Scurati affair, a European injury”

Maurizio Molinari: “the Scurati affair, a European injury” Irritable bowel syndrome: the effectiveness of low-carbohydrate diets is confirmed

Irritable bowel syndrome: the effectiveness of low-carbohydrate diets is confirmed Beware of the three main sources of poisoning in children

Beware of the three main sources of poisoning in children First three cases of “native” cholera confirmed in Mayotte

First three cases of “native” cholera confirmed in Mayotte Meningitis: compulsory vaccination for babies will be extended in 2025

Meningitis: compulsory vaccination for babies will be extended in 2025 When traveling abroad, money is a source of stress for seven out of ten French people

When traveling abroad, money is a source of stress for seven out of ten French people Elon Musk arrives in China to negotiate data transfer and deployment of Tesla autopilot

Elon Musk arrives in China to negotiate data transfer and deployment of Tesla autopilot Patrick Pouyanné, CEO of TotalEnergies, is very reserved about the rapid growth of green hydrogen

Patrick Pouyanné, CEO of TotalEnergies, is very reserved about the rapid growth of green hydrogen In the United States, a Boeing 767 loses its emergency slide shortly after takeoff

In the United States, a Boeing 767 loses its emergency slide shortly after takeoff A charred papyrus from Herculaneum reveals its secrets about Plato

A charred papyrus from Herculaneum reveals its secrets about Plato The watch of the richest passenger on the Titanic sold for 1.175 million pounds at auction

The watch of the richest passenger on the Titanic sold for 1.175 million pounds at auction Youn Sun Nah: jazz with nuance and delicacy

Youn Sun Nah: jazz with nuance and delicacy Paris Globe, a new international theater festival

Paris Globe, a new international theater festival Skoda Kodiaq 2024: a 'beast' plug-in hybrid SUV

Skoda Kodiaq 2024: a 'beast' plug-in hybrid SUV Tesla launches a new Model Y with 600 km of autonomy at a "more accessible price"

Tesla launches a new Model Y with 600 km of autonomy at a "more accessible price" The 10 best-selling cars in March 2024 in Spain: sales fall due to Easter

The 10 best-selling cars in March 2024 in Spain: sales fall due to Easter A private jet company buys more than 100 flying cars

A private jet company buys more than 100 flying cars This is how housing prices have changed in Spain in the last decade

This is how housing prices have changed in Spain in the last decade The home mortgage firm drops 10% in January and interest soars to 3.46%

The home mortgage firm drops 10% in January and interest soars to 3.46% The jewel of the Rocío de Nagüeles urbanization: a dream villa in Marbella

The jewel of the Rocío de Nagüeles urbanization: a dream villa in Marbella Rental prices grow by 7.3% in February: where does it go up and where does it go down?

Rental prices grow by 7.3% in February: where does it go up and where does it go down? Even on a mission for NATO, the Charles-de-Gaulle remains under French control, Lecornu responds to Mélenchon

Even on a mission for NATO, the Charles-de-Gaulle remains under French control, Lecornu responds to Mélenchon “Deadly Europe”, “economic decline”, immigration… What to remember from Emmanuel Macron’s speech at the Sorbonne

“Deadly Europe”, “economic decline”, immigration… What to remember from Emmanuel Macron’s speech at the Sorbonne Sale of Biogaran: The Republicans write to Emmanuel Macron

Sale of Biogaran: The Republicans write to Emmanuel Macron Europeans: “All those who claim that we don’t need Europe are liars”, criticizes Bayrou

Europeans: “All those who claim that we don’t need Europe are liars”, criticizes Bayrou These French cities that will boycott the World Cup in Qatar

These French cities that will boycott the World Cup in Qatar MLS: new double for Messi who offers victory to Miami

MLS: new double for Messi who offers victory to Miami PSG-Le Havre: Ramos on his way, Kolo Muani at the bottom of the hole… Favorites and scratches

PSG-Le Havre: Ramos on his way, Kolo Muani at the bottom of the hole… Favorites and scratches Football: Vasco da Gama separates from its Argentinian coach Ramon Diaz

Football: Vasco da Gama separates from its Argentinian coach Ramon Diaz F1: for the French, Ayrton Senna is the 2nd best driver in history ahead of Prost

F1: for the French, Ayrton Senna is the 2nd best driver in history ahead of Prost

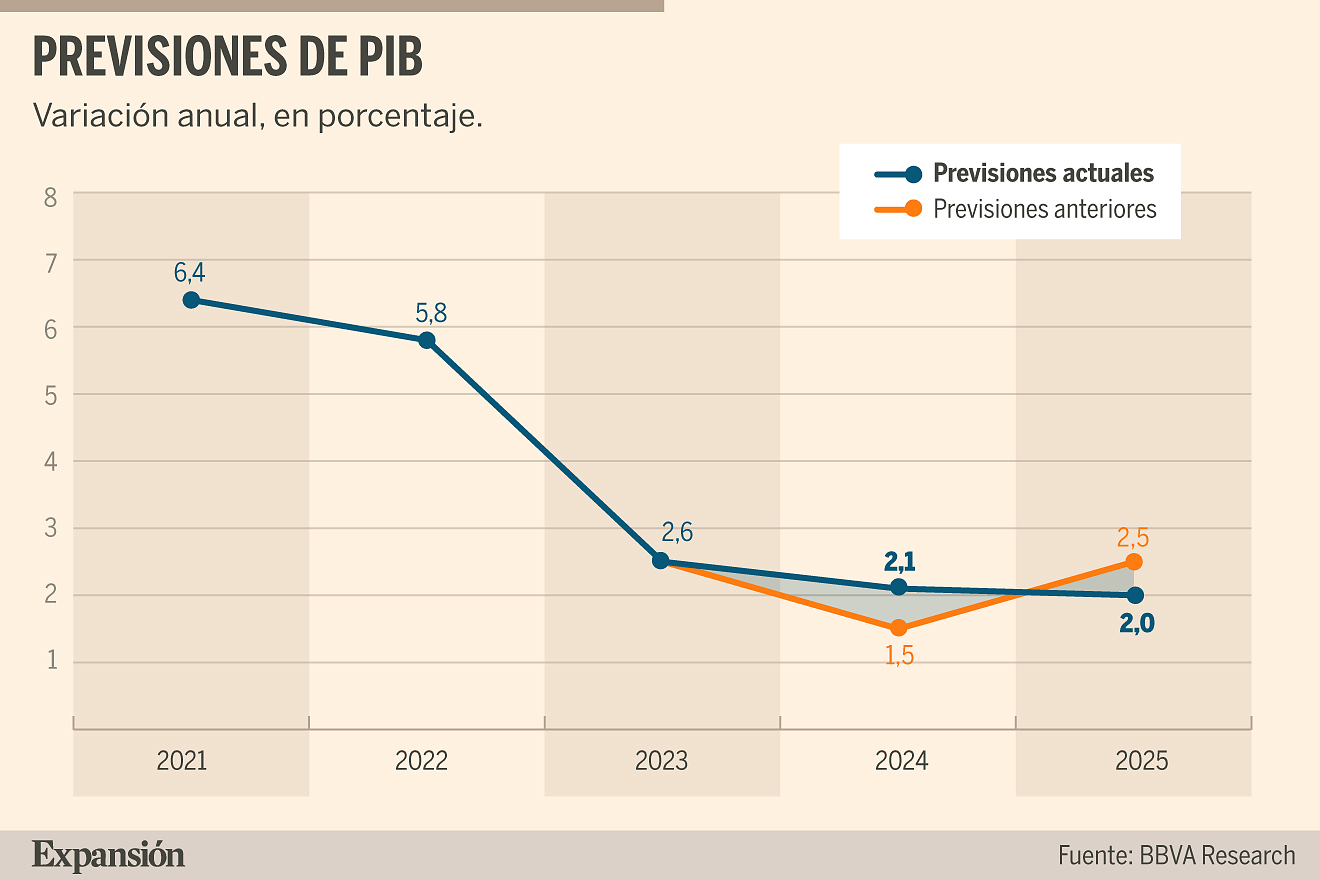

The Spanish economy is growing at a rate of 0.6% in the first quarter of this year, which in annualized terms would translate into an increase of 2.4% annually, as stated this Wednesday by the head of Economic Analysis at BBVA. Research, Rafael Doménech, who today presented in Madrid the Spain Situation report for the month of March carried out by the BBVA Research Service.

This quarterly increase in GDP of 0.6% would mean maintaining the same growth rate with which 2023 closed, since, according to data provided by the National Institute of Statistics (INE), yet to be confirmed, the Spanish economy registered in last quarter of last year a quarterly advance of 0.6%, three tenths more than in the previous quarter.

Macro indicators are positive for the evolution of the Spanish economy in the coming months, according to the study, although BBVA Research experts have warned that the weakness of private investment and productivity, the lack of qualified labor and Economic policy adds uncertainty to the economic scenario.

For 2025, BBVA Research has lowered its GDP growth forecast from 2.5% to 2.0% due to the foreseeable impact of the adjustment in public accounts demanded by Brussels and greater expected weakness of the eurozone economy.

The GDP has accelerated its growth rate in the final part of 2023 and the beginning of 2024, registering increases close to 0.5% quarterly.

Now, moving into the first quarter of 2024, "fiscal policy is being somewhat more expansive than expected, and the execution of European funds is reaching cruising speed," the study notes. Meanwhile, "the progress in Social Security affiliation shows a progressive improvement since October 2023, after the slowdown observed in the third quarter," explained Jorge Sicilia, Chief Economist of the BBVA Group and director of BBVA Research. .

Doménech has advanced in an interview with RNE that the Spanish economy, and also the European one, will benefit from the "timid" drops that some interest rates have begun to experience, such as the Euribor, and from the decline in the prices of oil and gas, which are "well below" the levels of a few quarters ago.

"Real-time information indicates that consumption continues to grow, both private consumption (0.5%, quarterly in the first quarter of 2024) and that of Public Administrations (0.2%)", and exports of goods and services also show better performance than expected, especially in a context of stagnation of economic activity in some of the main trading partners.

Likewise, industrial production seems to be recovering, driven by the disappearance of bottlenecks in the automotive sector, the reduction in the cost of energy and transportation, in addition to the inflection point in the supply of the agri-food sector.

BBVA Research economists highlight the recovery in service exports that has occurred since 2021, both in tourism and, above all, in the rest. "This has been helped by the change in family consumption habits since the pandemic, which has increased the weight of services in their spending," the economists point out. "This seems to be a shared trend in developed economies and explains, in part, that card spending by foreigners in Spain ahead of non-resident consumption would continue to advance significantly at the beginning of the year (5.6% quarterly in the first quarter of 2024).

The report also highlights that if the fall in the cost of energy is consolidated, it will mean improvements in competitiveness, especially in the electro-intensive industry and export companies. "Despite geopolitical tensions, the price of oil has fallen compared to the levels observed at the end of September. On the other hand, gas inventories remain high, thanks to the lack of dynamism of the European economy, favorable conditions and the returns on investments made in previous years. In total, it is estimated that these changes could add up to 0.4 percentage points to GDP growth in 2024."

In this context, inflation is declining and could reach 3.1% in 2024 (almost half a point below what was forecast in November) and 2.3% in 2025. Thus, the European Central Bank (ECB) will begin to reduce the monetary policy interest rate in June, six months earlier than expected in November. The decline in inflation, which is also observed in the rest of the eurozone, has been accompanied by some concern about the behavior of activity on the continent. The forecast for the end of the year indicates that the ECB could begin the process of reducing the monetary policy rate in the second quarter of the year, and bring it to 3.75% towards the end of 2024, completing a decrease of 75 basis points in total.

"Fiscal policy is being more expansive than expected," says BBVA Research. The formation of a new Government has not brought an agreement to have General State Budgets (PGE) since the beginning of the year. Likewise, the partial extension of tax reductions on the purchase of gas and electricity, in addition to the production of the latter, has been announced. In the same way, subsidies for the use of public transport are maintained.

"The latter measures will not be reversed, at the earliest, until June of this year. Meanwhile, the agreement reached on the new fiscal rules in the EMU has prevented the rules of the Stability and Growth Pact from coming into force again in 2024, which would have led to an immediate and important adjustment."

Economists perceive that the tenders and subsidies of the Transformation and Resilience Recovery Plan (PRTR) have reached cruising speed, which could be enough to fully execute the funds by 2026.

According to BBVA Research, since the beginning of the Plan and until the end of 2023, contracts have been put out to tender and subsidies financed with the Recovery and Resilience Mechanism (MRR) for an amount greater than 70,000 million euros, which represents more than 88 % of the total initially planned in the PRTR and in the Addendum transfers. However, they would have only been resolved, and therefore it is money that is already available to families and companies, more than 33.5 billion euros, which is equivalent to 42% of the total of the Plan.

BBVA Research estimates that, among the factors that could lead to greater growth in the coming months, is the additional decrease in production costs as a result of the investments that have been made to increase the supply of renewable energy and efficiency in the use of electricity.

It is also possible that there will be an acceleration in investment if reforms are consolidated to reduce the cost of some procedures, especially in the real estate sector.

In addition, there remains a stagnant demand for transportation equipment, which could resurface to the extent that uncertainty regarding the acquisition of electric vehicles is reduced. Finally, immigration could continue and, to the extent that it is complementary to human capital residing in Spain, boost employment and productivity.

With respect to the labor market, BBVA Research observes that various supply restrictions remain that will limit the advancement of employment. Immigration and the increase in the activity rate have allowed job creation to continue.

However, they do not appear to have helped improve productivity. "This may be a symptom that it remains difficult to find certain profiles in industries and services with high added value."

Additionally, the aging population is reducing the availability of working-age workers. This is added to the surprising decrease that has been occurring in the participation rate of Spaniards between 35 and 54 years old. "In the absence of policies that improve the employability of these workers or an immigration policy that attracts human capital complementary to that of residents in Spain, these factors can be a bottleneck for growth," they point out.

"Policies to boost housing demand or price fixing can have harmful long-term effects on the sector," says BBVA Research. The Government has announced guarantees for young people, through the Official Credit Institute (ICO), with the aim of facilitating access to housing. But economists understand that the measure suffers from several problems.

On the one hand, "it is designed with the same defects that afflict others and that can generate inequality. By placing rigid limits on age (35 years), income (37,800 euros annually) or to request credit (December 31 2024), discrimination is made against those people who barely overcome these barriers (or who want to buy from 2025 onwards)".

Likewise, "it is very possible that the measure will end up benefiting young people who currently earn less than the specified income, but who in the future will have incomes above the average."

"Although limits are required on the wealth accumulated by buyers, the same is not required for that of parents, which, again, could end up favoring high-income households."

Another problem is that "it is not advisable to encourage loans that finance 100% of the value of the home, since it can lead to an increase in the risk taking of financial entities."

"And finally, and most importantly, without policies that increase the supply of housing, purchase aid will lead to increases in prices, without improving accessibility for young people. The same will happen with policies to fix the cost of rent, which They can even encourage exit from the housing market," the economists point out.

BBVA Research economists fear that by 2025 the slowdown in growth in certain sectors and countries in the eurozone will be more structural than initially thought. The German economy has shown practically no progress for two years. The French company's improvement is meager if the high imbalance in its public accounts is taken into account.

"The industrial export growth model seems exhausted. In both Spain and Germany, the companies that have had the worst performance are those that are intensive in the use of energy or that are part of the same value chain. Likewise, in an environment of consolidation fiscal and, still, with high interest rates, it will be difficult for the internal demand of countries with deficits above 3% of GDP to contribute to growth.

In parallel, the new fiscal rules in Europe will require important and sustained adjustments over time in several economies, including Spain, starting in 2025. Countries such as France, Spain or Italy, with deficits greater than 3% of GDP and levels of public debt above 90% will have to commit to implementing structural consolidation measures between 0.4 and 0.6 percentage points of GDP per year.

In the case of Spain, the forecasts foresee a structural adjustment of 0.5 percentage points of GDP in 2025, which, together with the expected economic recovery, would take the public deficit to 2.9% of GDP at the end of the following year. and the debt, at 102% of GDP.

The BBVA Research Service has lowered the estimated GDP growth for Spain in 2025 from 2.5% to 2.0%, due to the need to begin the adjustment in public accounts and the greater expected weakness of the economy of the eurozone. Added to this is the poor performance of investment in Spain, especially in comparison with what is observed in the rest of the eurozone.

Likewise, productivity is expected to stagnate and labor costs to increase, which may limit employment growth. BBVA Research observes that supply restrictions persist due to the lack of qualified labor or regulation, which prevents the growth of the supply of housing, especially affordable housing. Finally, they estimate that economic policy uncertainty will remain high.