Germany: Man armed with machete enters university library and threatens staff

Germany: Man armed with machete enters university library and threatens staff His body naturally produces alcohol, he is acquitted after a drunk driving conviction

His body naturally produces alcohol, he is acquitted after a drunk driving conviction Who is David Pecker, the first key witness in Donald Trump's trial?

Who is David Pecker, the first key witness in Donald Trump's trial? What does the law on the expulsion of migrants to Rwanda adopted by the British Parliament contain?

What does the law on the expulsion of migrants to Rwanda adopted by the British Parliament contain? Parvovirus alert, the “fifth disease” of children which has already caused the death of five babies in 2024

Parvovirus alert, the “fifth disease” of children which has already caused the death of five babies in 2024 Colorectal cancer: what to watch out for in those under 50

Colorectal cancer: what to watch out for in those under 50 H5N1 virus: traces detected in pasteurized milk in the United States

H5N1 virus: traces detected in pasteurized milk in the United States What High Blood Pressure Does to Your Body (And Why It Should Be Treated)

What High Blood Pressure Does to Your Body (And Why It Should Be Treated) Insurance: SFAM, subsidiary of Indexia, placed in compulsory liquidation

Insurance: SFAM, subsidiary of Indexia, placed in compulsory liquidation Under pressure from Brussels, TikTok deactivates the controversial mechanisms of its TikTok Lite application

Under pressure from Brussels, TikTok deactivates the controversial mechanisms of its TikTok Lite application “I can’t help but panic”: these passengers worried about incidents on Boeing

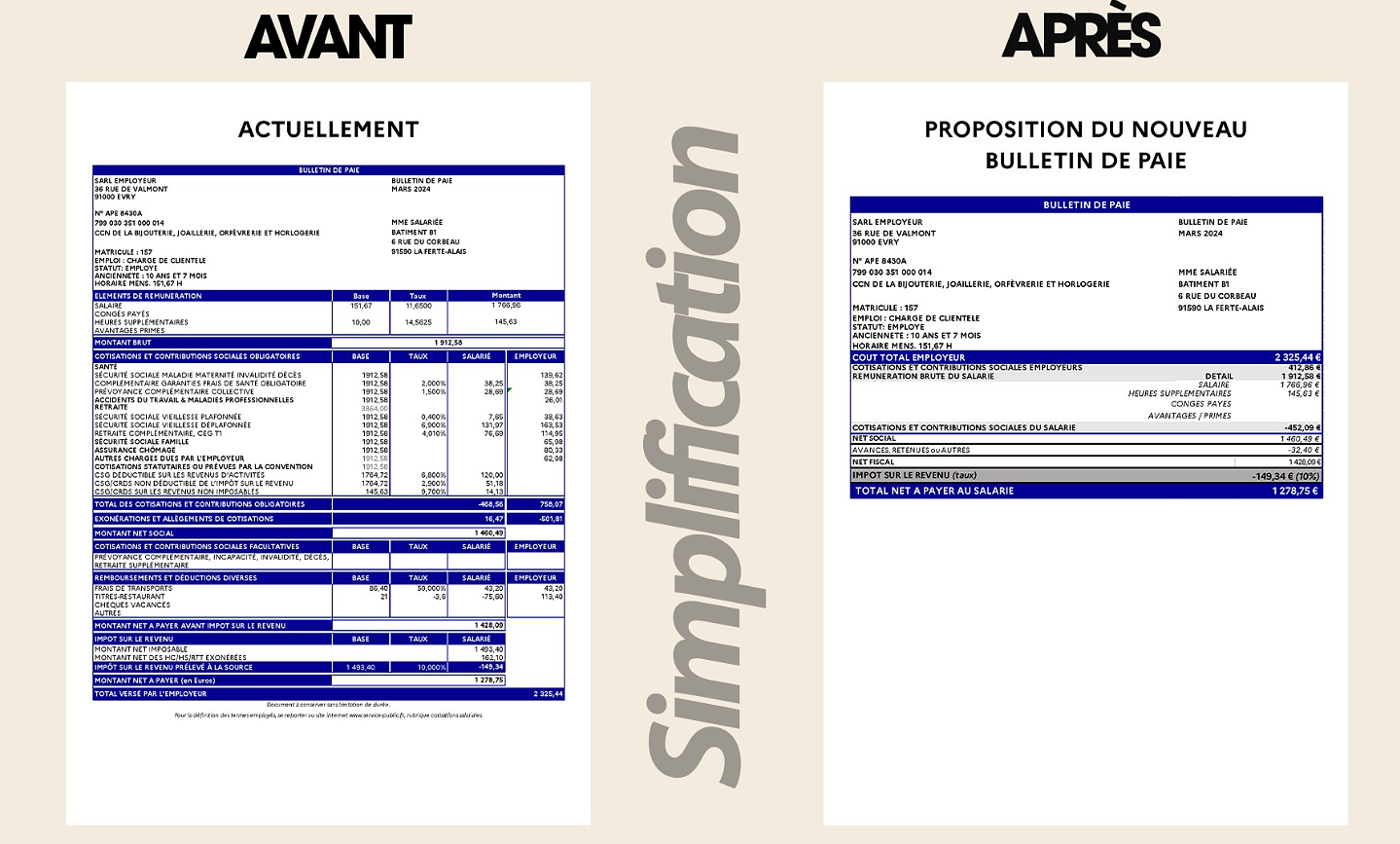

“I can’t help but panic”: these passengers worried about incidents on Boeing “I’m interested in knowing where the money that the State takes from me goes”: Bruno Le Maire’s strange pay slip sparks controversy

“I’m interested in knowing where the money that the State takes from me goes”: Bruno Le Maire’s strange pay slip sparks controversy 25 years later, the actors of Blair Witch Project are still demanding money to match the film's record profits

25 years later, the actors of Blair Witch Project are still demanding money to match the film's record profits At La Scala, Mathilde Charbonneaux is Madame M., Jacqueline Maillan

At La Scala, Mathilde Charbonneaux is Madame M., Jacqueline Maillan Deprived of Hollywood and Western music, Russia gives in to the charms of K-pop and manga

Deprived of Hollywood and Western music, Russia gives in to the charms of K-pop and manga Exhibition: Toni Grand, the incredible odyssey of a sculptural thinker

Exhibition: Toni Grand, the incredible odyssey of a sculptural thinker Skoda Kodiaq 2024: a 'beast' plug-in hybrid SUV

Skoda Kodiaq 2024: a 'beast' plug-in hybrid SUV Tesla launches a new Model Y with 600 km of autonomy at a "more accessible price"

Tesla launches a new Model Y with 600 km of autonomy at a "more accessible price" The 10 best-selling cars in March 2024 in Spain: sales fall due to Easter

The 10 best-selling cars in March 2024 in Spain: sales fall due to Easter A private jet company buys more than 100 flying cars

A private jet company buys more than 100 flying cars This is how housing prices have changed in Spain in the last decade

This is how housing prices have changed in Spain in the last decade The home mortgage firm drops 10% in January and interest soars to 3.46%

The home mortgage firm drops 10% in January and interest soars to 3.46% The jewel of the Rocío de Nagüeles urbanization: a dream villa in Marbella

The jewel of the Rocío de Nagüeles urbanization: a dream villa in Marbella Rental prices grow by 7.3% in February: where does it go up and where does it go down?

Rental prices grow by 7.3% in February: where does it go up and where does it go down? Sale of Biogaran: The Republicans write to Emmanuel Macron

Sale of Biogaran: The Republicans write to Emmanuel Macron Europeans: “All those who claim that we don’t need Europe are liars”, criticizes Bayrou

Europeans: “All those who claim that we don’t need Europe are liars”, criticizes Bayrou With the promise of a “real burst of authority”, Gabriel Attal provokes the ire of the opposition

With the promise of a “real burst of authority”, Gabriel Attal provokes the ire of the opposition Europeans: the schedule of debates to follow between now and June 9

Europeans: the schedule of debates to follow between now and June 9 These French cities that will boycott the World Cup in Qatar

These French cities that will boycott the World Cup in Qatar Tennis: 1000 matches and 10 notable encounters by Richard Gasquet

Tennis: 1000 matches and 10 notable encounters by Richard Gasquet Tennis: first victory of the season on clay for Osaka in Madrid

Tennis: first victory of the season on clay for Osaka in Madrid La Rochelle-Toulon: at what time and on which channel to follow the closing match of the 22nd day of Top 14

La Rochelle-Toulon: at what time and on which channel to follow the closing match of the 22nd day of Top 14 Ligue 2: Dunkirk accuses a Girondins de Bordeaux player of racist insults

Ligue 2: Dunkirk accuses a Girondins de Bordeaux player of racist insults

Who goes in the next few years in Pension, must reckon with a significantly lower pension from the pension Fund than today's pensioners. The long-sustained low interest rates lead to the fact that the age balance of the 2. Pillar to rise more slowly. Secondly, some funds have lowered the conversion rate, or even the pensions lessen in addition.

Many can not afford to make voluntary payments into the pension Fund, in order to improve the services. And those who can afford it, do not need to be aware that deposits have in every case positive; in addition, there are legal barriers. Shopping willing should note the following aspects:

pension gap: Voluntary payments into the pension Fund are only possible, if the pension gap is. Most Fund certificate in the annual personal Pension, whether that is the case or how high the maximum purchase amount is. to determine

the pension gap, make the pension Fund a hypothetical calculation, says Heinz Barmettler from the Federal social insurance office. The Fund from the current wage of the insured Person and see how much the Person would have on the old account, if you would have had these wage from the age of 25 years. "Is the hypothetical savings to be greater than the actual, corresponds to the difference of the pension gap."

Legal requirements: Who has financed with the pension funds of their own home, this covers only completely pay back, before he can buy. Even those who have deposited in a vested benefits account-other pension funds, it must state this, says Barmettler. As a result, the potential Purchase price reduces accordingly.

Where the shopping is: A Central question is how the Fund accounts for the purchase amount. the pension funds that offer more than the statutory Obligation, set this yourself. You could split the amount between the mandatory and non-mandatory balances or him entirely to the Überobligatorium allocate, so Barmettler.

What sounds very technical, has a direct impact on the services. The Fund accounts for the purchase amount only in the extra-mandatory assets, there is no legally guaranteed minimum interest rate. Also, the conversion rate, the pension is calculated, is in the Überobligatorium usually significantly lower than in Mandatory. There, the law requires 6.8 percent. This can lead to the old-age pension is, in spite of of shopping is hardly bigger. To avoid unpleasant Surprises, should the Insured be informed in advance of how the Fund accounts for the purchase and what terms and conditions apply.

death before the pension age: What happens with the voluntary contributions, if the insured Person dies before Retirement? Also, each Fund establishes itself, the law makes no specifications. In General, the money will be used to improve the pensions of widows or orphans, says pension Fund expert Liliane Grossmann, who sits on the Board of the Association of BVG information. While many of the funds disbursed today, the shopping amounts of the surviving bar. Nevertheless, Grossmann advises this in a timely manner to clarify.

beware of under cover: is Also the financial Situation of the pension Fund, it is important to check. Appropriate information obtained from the annual report or the Board of Trustees of the Fund. Critical about the degree of coverage is. This is significantly below 100 percent, it means: be careful, says Liliane Grossmann. "There is the risk that the Insured in the reorganization will need to participate", which could diminish the value of the voluntary payments is.

date of purchase: the money Is in the pension Fund, it stays there until Retirement. Early withdrawals are only possible in exceptional cases – such as for the financing of residential property. Therefore, purchases are only from the age of 50 years. "Otherwise, the capital is tied up for too long," says Karl Flubacher, business head North-West Region and Western Switzerland to the VZ wealth center. In addition, there is in the 2. Pillar is currently a redistribution. Active Insured had to accept losses, so that the pensions of the Retired could be financed. Also, this speaks loudly Flubacher for purchases not too early to make. Note, however, that deposits, which are held for less than three years prior to Retirement, can only be used as a pension.

save on taxes: A major advantage of voluntary deposits are the savings in taxes. Purchases in the 2. Pillar can be deducted from taxable income. Flubacher recommends that larger amounts at least to several years to split. "So more taxes can usually save more than if you pay everything on Time."

Preparedness expert Karl Flubacher is convinced that Well-prepared, be it useful, in the pension Fund to shop. He adds: "While one could increase the old-age pension, today it is mostly only the possession of state."

Created: 01.12.2019, 19:12 PM