Germany: Man armed with machete enters university library and threatens staff

Germany: Man armed with machete enters university library and threatens staff His body naturally produces alcohol, he is acquitted after a drunk driving conviction

His body naturally produces alcohol, he is acquitted after a drunk driving conviction Who is David Pecker, the first key witness in Donald Trump's trial?

Who is David Pecker, the first key witness in Donald Trump's trial? What does the law on the expulsion of migrants to Rwanda adopted by the British Parliament contain?

What does the law on the expulsion of migrants to Rwanda adopted by the British Parliament contain? Parvovirus alert, the “fifth disease” of children which has already caused the death of five babies in 2024

Parvovirus alert, the “fifth disease” of children which has already caused the death of five babies in 2024 Colorectal cancer: what to watch out for in those under 50

Colorectal cancer: what to watch out for in those under 50 H5N1 virus: traces detected in pasteurized milk in the United States

H5N1 virus: traces detected in pasteurized milk in the United States What High Blood Pressure Does to Your Body (And Why It Should Be Treated)

What High Blood Pressure Does to Your Body (And Why It Should Be Treated) Insurance: SFAM, subsidiary of Indexia, placed in compulsory liquidation

Insurance: SFAM, subsidiary of Indexia, placed in compulsory liquidation Under pressure from Brussels, TikTok deactivates the controversial mechanisms of its TikTok Lite application

Under pressure from Brussels, TikTok deactivates the controversial mechanisms of its TikTok Lite application “I can’t help but panic”: these passengers worried about incidents on Boeing

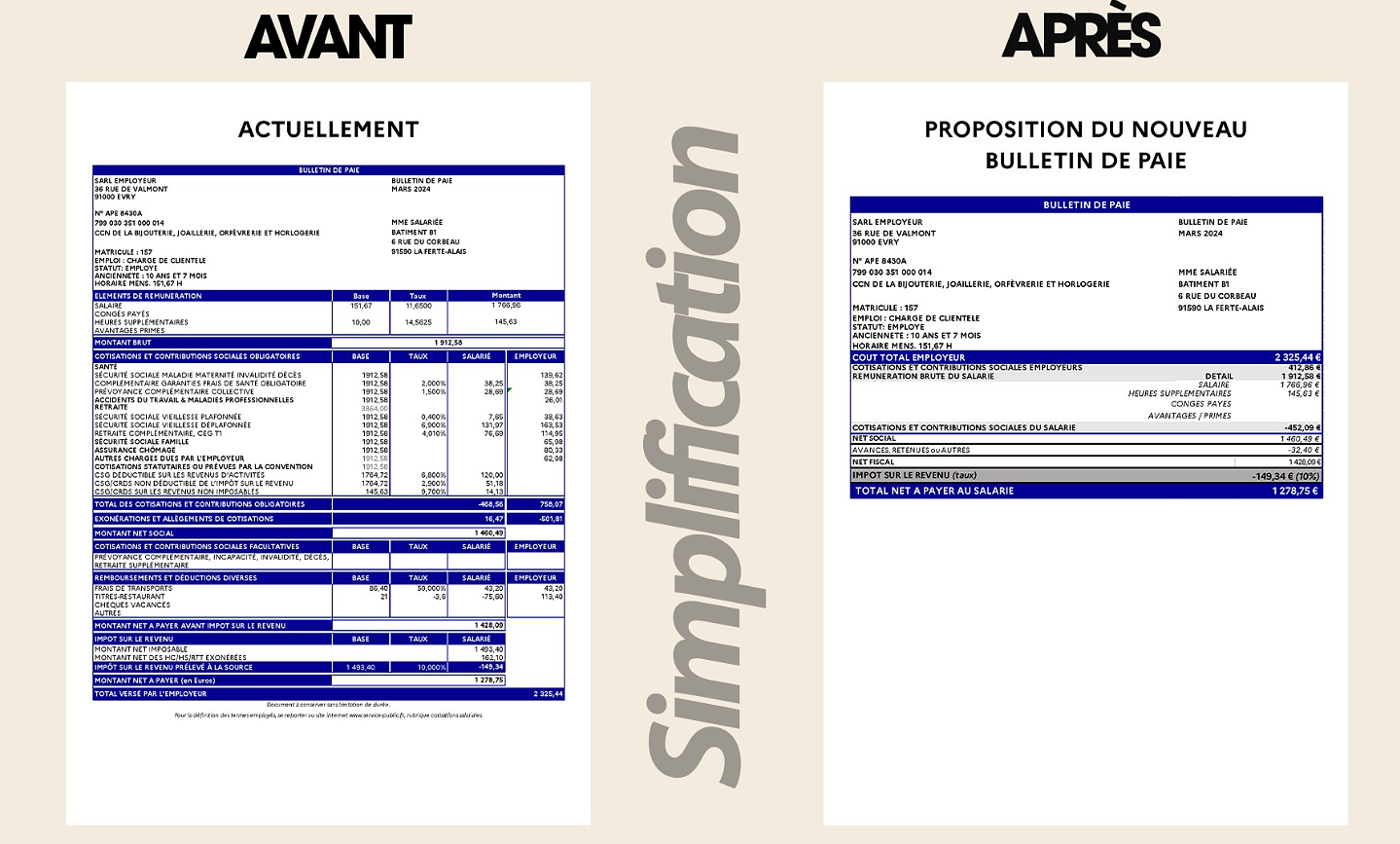

“I can’t help but panic”: these passengers worried about incidents on Boeing “I’m interested in knowing where the money that the State takes from me goes”: Bruno Le Maire’s strange pay slip sparks controversy

“I’m interested in knowing where the money that the State takes from me goes”: Bruno Le Maire’s strange pay slip sparks controversy 25 years later, the actors of Blair Witch Project are still demanding money to match the film's record profits

25 years later, the actors of Blair Witch Project are still demanding money to match the film's record profits At La Scala, Mathilde Charbonneaux is Madame M., Jacqueline Maillan

At La Scala, Mathilde Charbonneaux is Madame M., Jacqueline Maillan Deprived of Hollywood and Western music, Russia gives in to the charms of K-pop and manga

Deprived of Hollywood and Western music, Russia gives in to the charms of K-pop and manga Exhibition: Toni Grand, the incredible odyssey of a sculptural thinker

Exhibition: Toni Grand, the incredible odyssey of a sculptural thinker Skoda Kodiaq 2024: a 'beast' plug-in hybrid SUV

Skoda Kodiaq 2024: a 'beast' plug-in hybrid SUV Tesla launches a new Model Y with 600 km of autonomy at a "more accessible price"

Tesla launches a new Model Y with 600 km of autonomy at a "more accessible price" The 10 best-selling cars in March 2024 in Spain: sales fall due to Easter

The 10 best-selling cars in March 2024 in Spain: sales fall due to Easter A private jet company buys more than 100 flying cars

A private jet company buys more than 100 flying cars This is how housing prices have changed in Spain in the last decade

This is how housing prices have changed in Spain in the last decade The home mortgage firm drops 10% in January and interest soars to 3.46%

The home mortgage firm drops 10% in January and interest soars to 3.46% The jewel of the Rocío de Nagüeles urbanization: a dream villa in Marbella

The jewel of the Rocío de Nagüeles urbanization: a dream villa in Marbella Rental prices grow by 7.3% in February: where does it go up and where does it go down?

Rental prices grow by 7.3% in February: where does it go up and where does it go down? Sale of Biogaran: The Republicans write to Emmanuel Macron

Sale of Biogaran: The Republicans write to Emmanuel Macron Europeans: “All those who claim that we don’t need Europe are liars”, criticizes Bayrou

Europeans: “All those who claim that we don’t need Europe are liars”, criticizes Bayrou With the promise of a “real burst of authority”, Gabriel Attal provokes the ire of the opposition

With the promise of a “real burst of authority”, Gabriel Attal provokes the ire of the opposition Europeans: the schedule of debates to follow between now and June 9

Europeans: the schedule of debates to follow between now and June 9 These French cities that will boycott the World Cup in Qatar

These French cities that will boycott the World Cup in Qatar Hand: Montpellier crushes Kiel and continues to dream of the Champions League

Hand: Montpellier crushes Kiel and continues to dream of the Champions League OM-Nice: a spectacular derby, Niçois timid despite their numerical superiority...The tops and the flops

OM-Nice: a spectacular derby, Niçois timid despite their numerical superiority...The tops and the flops Tennis: 1000 matches and 10 notable encounters by Richard Gasquet

Tennis: 1000 matches and 10 notable encounters by Richard Gasquet Tennis: first victory of the season on clay for Osaka in Madrid

Tennis: first victory of the season on clay for Osaka in Madrid

economic growth per capita has been weak in recent years, and we now have a place on the weaker, however, among the countries of Europe. This mediocre result may be partly explained by the fact that we become more through the wave and of the structural fault in the Swedish economy, but is likely also of the conduct of monetary policy.

How good is it really possible for Swedish companies as the engine behind the growth? The stock market trend with a rise in the OMX-index of over 30 percent in the last five years broadcasting definitely no krissignal. But in the light of the conduct of monetary policy, we have every reason to ask ourselves if the stock market really reflect how the competitiveness of Swedish companies.

. Sure, you might think that it is a perfect world for a company to work with a virtually ”free” capital, and with a kronutveckling därden american dollars gone from the six crowns after the financial crisis, to just over nine dollars now and where this development has no equivalent in the rate of inflation between the countries. Everyone understands the difference in getting the home to nine million instead of six million for a contract of sale of a million dollars. To this pure translation should be ”the help” from the exchange rate, which can be used in the price competition. One can simply dispense a little of the profit you make on the exchange rate, and lowering the price in dollars and thus beat out an american competitor, at his home.

A more conspiratorial explanation for the low transparency is that management is controlled by an asymmetric incentive system that leads to the bonus at the macro-economic tail wind, and no punishment at the headwind.

however, It is not only the export industry which is the winner. Large parts of the domestic business is also helped by the contribution from the exchange rate, which is supposed to more expensive imports, and helping to bring inflation up. This means that the foreign exporters to Sweden sells smaller volumes and Swedish companies are thus given an opportunity to increase their sales. In other words, is this protectionism packaged as deflationsbekämpning and with the greater part of the Swedish business community as the winner.

This provides companies not only with cheap capital but, more importantly, an increased demand for capital-intensive products.

There is thus every reason to ask how large a share of the profits in our businesses that will be left when the macroeconomic tailwind mojnar and turn into a headwind?

the Historical example shows that the macro-economic head and tail wind affect the pressure on efficiency and innovation in companies. The experience of the united states in the early 1980s, gives us a warning in this respect. Dollar an overvaluation then gradually and was in the beginning of 1985 overvalued by about 50%. This all for high score meant that production in the U.S. was coated with something that can be likened to ”a tax” of this size.

His argument was that Europe would become frånåkt of the american business community if you exposed it for an overvalued currency in this order of magnitude. With the whip on the back would american companies are forced to restructure and rationalise and become more competitive. European companies would fall behind in the global market. He was absolutely right and, 20 years later, ”forced” the EU to establish the Lisbon strategy with the aim to catch up with the united states competitively.

the Lesson of this is that the pressure in the form of macroeconomic headwinds lead to higher pressures. Macroeconomic tailwind on the other hand, leads to decreased efforts to improve the efficiency and thus improve competitiveness. The aggressiveness of the improvements is slowing.

What do we know about the development? Unfortunately, gives today's annual and quarterly reports, no answer to the question, and without information from the companies, it is not possible to get an overview of how competitiveness has been developed. This is basically not specific for Swedish companies, but there is a generally poor transparency in this area, which I described in a recently published scientific study of Europe's hundred largest companies. What distinguishes Sweden is the extraordinary strength of the macro-economic tailwind.

One explanation may be that the information on the high cost can end up of competitors who can take advantage of it. This would be a key explanation to the lack of transparency in Swedish companies, however, is not likely. Perhaps it is rather that the management and board of directors do not realize the problem due to the training in macroeconomics and business administration has always been in the siloform. Many companies are hiding incorrectly behind the declaration that the company's business is so global that everything evens itself out.

A more conspiratorial explanation for the low transparency is that management is controlled by an asymmetric incentive system that leads to the bonus at the macro-economic tail wind, and no punishment at the headwind. Get the feel then attracted to forgo a bonus for the shareholders describe a reported vinstuppgång at 20% – after that is taken into account that the company had a macro-economic tail wind of 30 per cent during the period – a de facto loss of competitiveness of 10 per cent.

Valutadelen in the tailwind for the companies is an uphill battle for the individual citizen in the short term, whose such as holidays abroad become more expensive. The purpose of the policy is that, in the longer term, lead to a better society, the individual will benefit. But if the macroeconomic tailwind always store away, and the competitiveness of the Swedish business sector falls, the positive effects for the individual never materialized.

The economic support that the majority of Swedish companies scored by the Riksbank and the economic policy during the last ten years is risky in a longer perspective. Today, there is every reason for shareholders and employees as well as for our politicians to ask the question, how competitiveness is actually developed? Without the pressure from different stakeholder groups to get an answer to this question is a serious risk that pressures and efficiency in Swedish companies is slowing due to the macroeconomic tailwind. Sweden will therefore as a nation – much like Europe during the 1980s – falling behind the united states and other nations on the global stage. Despite positive signals from the stock market is the current low growth, perhaps a first sign that the descent started.