Germany: Man armed with machete enters university library and threatens staff

Germany: Man armed with machete enters university library and threatens staff His body naturally produces alcohol, he is acquitted after a drunk driving conviction

His body naturally produces alcohol, he is acquitted after a drunk driving conviction Who is David Pecker, the first key witness in Donald Trump's trial?

Who is David Pecker, the first key witness in Donald Trump's trial? What does the law on the expulsion of migrants to Rwanda adopted by the British Parliament contain?

What does the law on the expulsion of migrants to Rwanda adopted by the British Parliament contain? Parvovirus alert, the “fifth disease” of children which has already caused the death of five babies in 2024

Parvovirus alert, the “fifth disease” of children which has already caused the death of five babies in 2024 Colorectal cancer: what to watch out for in those under 50

Colorectal cancer: what to watch out for in those under 50 H5N1 virus: traces detected in pasteurized milk in the United States

H5N1 virus: traces detected in pasteurized milk in the United States What High Blood Pressure Does to Your Body (And Why It Should Be Treated)

What High Blood Pressure Does to Your Body (And Why It Should Be Treated) Insurance: SFAM, subsidiary of Indexia, placed in compulsory liquidation

Insurance: SFAM, subsidiary of Indexia, placed in compulsory liquidation Under pressure from Brussels, TikTok deactivates the controversial mechanisms of its TikTok Lite application

Under pressure from Brussels, TikTok deactivates the controversial mechanisms of its TikTok Lite application “I can’t help but panic”: these passengers worried about incidents on Boeing

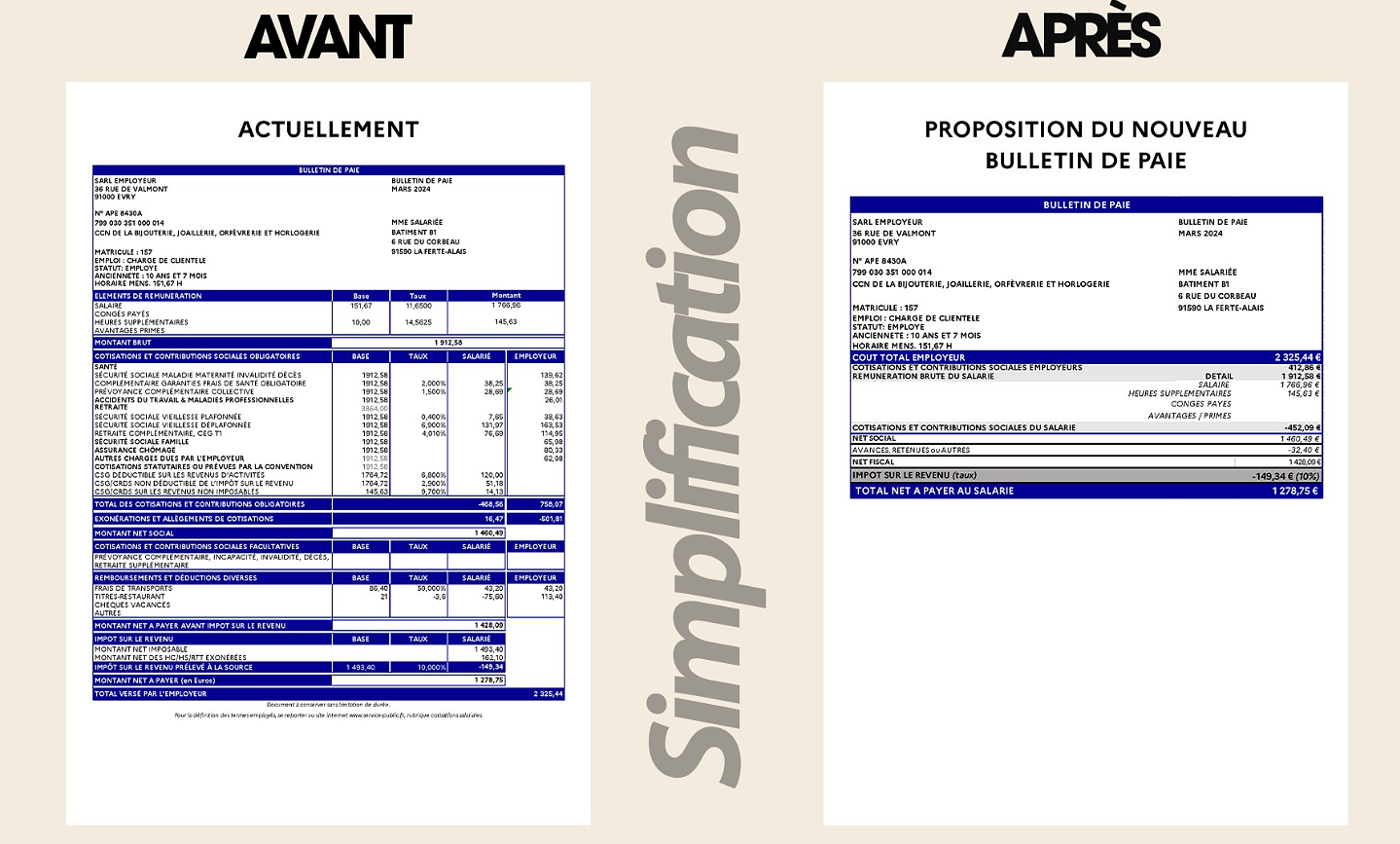

“I can’t help but panic”: these passengers worried about incidents on Boeing “I’m interested in knowing where the money that the State takes from me goes”: Bruno Le Maire’s strange pay slip sparks controversy

“I’m interested in knowing where the money that the State takes from me goes”: Bruno Le Maire’s strange pay slip sparks controversy 25 years later, the actors of Blair Witch Project are still demanding money to match the film's record profits

25 years later, the actors of Blair Witch Project are still demanding money to match the film's record profits At La Scala, Mathilde Charbonneaux is Madame M., Jacqueline Maillan

At La Scala, Mathilde Charbonneaux is Madame M., Jacqueline Maillan Deprived of Hollywood and Western music, Russia gives in to the charms of K-pop and manga

Deprived of Hollywood and Western music, Russia gives in to the charms of K-pop and manga Exhibition: Toni Grand, the incredible odyssey of a sculptural thinker

Exhibition: Toni Grand, the incredible odyssey of a sculptural thinker Skoda Kodiaq 2024: a 'beast' plug-in hybrid SUV

Skoda Kodiaq 2024: a 'beast' plug-in hybrid SUV Tesla launches a new Model Y with 600 km of autonomy at a "more accessible price"

Tesla launches a new Model Y with 600 km of autonomy at a "more accessible price" The 10 best-selling cars in March 2024 in Spain: sales fall due to Easter

The 10 best-selling cars in March 2024 in Spain: sales fall due to Easter A private jet company buys more than 100 flying cars

A private jet company buys more than 100 flying cars This is how housing prices have changed in Spain in the last decade

This is how housing prices have changed in Spain in the last decade The home mortgage firm drops 10% in January and interest soars to 3.46%

The home mortgage firm drops 10% in January and interest soars to 3.46% The jewel of the Rocío de Nagüeles urbanization: a dream villa in Marbella

The jewel of the Rocío de Nagüeles urbanization: a dream villa in Marbella Rental prices grow by 7.3% in February: where does it go up and where does it go down?

Rental prices grow by 7.3% in February: where does it go up and where does it go down? Sale of Biogaran: The Republicans write to Emmanuel Macron

Sale of Biogaran: The Republicans write to Emmanuel Macron Europeans: “All those who claim that we don’t need Europe are liars”, criticizes Bayrou

Europeans: “All those who claim that we don’t need Europe are liars”, criticizes Bayrou With the promise of a “real burst of authority”, Gabriel Attal provokes the ire of the opposition

With the promise of a “real burst of authority”, Gabriel Attal provokes the ire of the opposition Europeans: the schedule of debates to follow between now and June 9

Europeans: the schedule of debates to follow between now and June 9 These French cities that will boycott the World Cup in Qatar

These French cities that will boycott the World Cup in Qatar Hand: Montpellier crushes Kiel and continues to dream of the Champions League

Hand: Montpellier crushes Kiel and continues to dream of the Champions League OM-Nice: a spectacular derby, Niçois timid despite their numerical superiority...The tops and the flops

OM-Nice: a spectacular derby, Niçois timid despite their numerical superiority...The tops and the flops Tennis: 1000 matches and 10 notable encounters by Richard Gasquet

Tennis: 1000 matches and 10 notable encounters by Richard Gasquet Tennis: first victory of the season on clay for Osaka in Madrid

Tennis: first victory of the season on clay for Osaka in Madrid

Finma is ten years old. And the criticism is getting louder and louder. Now was adopted in Parliament with a Motion to review the powers of the Finma. Prepares you Worried?

A strong financial place needs a strong oversight. To do this, we need the appropriate instruments. The looks of the policy. I do not think, therefore, that the Federal Finma wants to take away skills. And criticism for a Supervisory authority to the business, cyclical time, more or less.

The cantonal banks, the Finma Excesses in the regulation. What do you say?

The regulation, for which we are responsible, is less grown than the underlying regulations and laws. And very much less than the regulation in the foreign countries. In comparison, our regulation is downright slim.

Where please is slim, the Finma regulation?

Take the topic of cyber risks. We have dealt with in just one and a half pages. The EU needs 66 pages, United States 41. But it is certainly the case that after the financial crisis, regulation is more strict, on all of the major financial centres. It is also true that the complexity has increased. We recognize that by differentiating the General Size of the Institute, and a special regime with far-reaching exemptions for small institutions grant, which is unique in the world.

"Our biggest concern is the real estate market, specifically the so-called investment properties."

countries such as the USA and the UK want to give their banks more freedom. Switzerland there is a danger of falling back?

The rules adopted by the Swiss Parliament after the crisis, in particular with a view on the capital provisions, the banking system have been made much safer. Because nothing should be turned back. But also in the USA and the UK has not changed for system-relevant banks in terms of regulation a lot. Therefore, I also see a new competitive disadvantage for Swiss banks.

oversee the entire financial sector. Where are the hidden currently, the biggest risks?

Us to make the low interest rate environment and its consequences. The low interest rates, insurers weigh on the classical banking business and also life. At the same time, low interest rates fuel the search for yield. Here our biggest concern is the real estate market, specifically the so-called investment properties.

And the second concern?

cyber risk give us big headaches, because the financial sector is interconnected technologically and, therefore, always vulnerable.

"In the case of a health insurer, but already a lot of customers lost data."

there Was already a Bank for a successful Hacking attack?

There are successful attacks, but they happen mostly to single customers. So far, we have had the luck of no case in which a Bank by a hacker's attack to a standstill or solid data has been lost. In the case of a health insurer, many customers have been lost already data. Overall, Switzerland came but, so far, unscathed. The sensitivity in this country is high, but the risk is also high. We should not lull us in a false sense of security.

a national Cyber skills centre is Missing, in your view?

Yes. If we look at how other countries deal with cyber risks, then Switzerland has catching up to do. Other countries with major financial centers make considerably more. We must not be naïve.

What do you mean?

the topic of Cyber not only to crime but also to attacks by state Authorities or attacks by terrorists. The issue touches on national security. Therefore, it should not go so much about where, exactly, such a competence centre of the Confederation is settled, but that it comes quickly and that it will be closely coordinated with the private sector. International cooperation helps here, by the way, because in the States trust each other well enough.

"The prices for investment properties are rising, but Rents are dropping, and vacancies are at record levels."

As a further risk, you of languages, the low level of interest rates. Are banks sufficiently prepared, when interest rates rise again?

More than the Exposure of their own balance sheets against rising interest rates the risk of loan default makes me in the mortgage market. The sustainable quality of the debtor in order to drives us, especially in the financing of investment objects. The prices are on the rise here, but Rents are dropping, and vacancies are at a record level. It, Switzerland is so far the same number of empty dwellings the number of dwellings in the Canton of Schwyz. And it will continue to built brisk. Should there be a correction, and should be loans, the banks will be able to absorb the losses.

you Have banks the Finger on knock?

We have repeatedly disposed of capital surcharges.

In the case of the anti-money laundering, you work with a red list of institutions that respond to high risks. Is the list longer?

The list is dynamic. There are usually around twenty institutions. With the list we want to help new scandals to prevent it, by acting where we see, for example, due to the population of Customers special risks.

cases such as the scandal of the Malaysian state Fund or the Venezuelan PDVSA are slipped through?

The cases are from the time before 2015. The effect of our intensive supervision shows in the next few years. Then I hope there are no scandals in this Dimension. And we see positive signs in the banks, they have become more cautious and to report suspected cases.

In a large money laundering case around the Danske Bank should, however, be again landed 12 billion Swiss francs in Switzerland.

Yes, 12 out of about 200 billion Swiss francs. 94 percent are of a different flowed where. The case shows, in other words: money laundering is an international and not a Switzerland-specific Problem.

What are the Swiss banks were a little cautious?

If this is the case, let's look at.

The case of Raiffeisen-chief Vincenz was the least of their greatest case. It is now Julius Baer?

you are on the fish! to Raiffeisen

Then. Why do you propose that the Central is a joint stock company?

We have made an open question. It comes to clarify whether the corporate governance and resolution planning in this Headquarters as a Corporation or as a cooperative easier. We make sure the co-operative idea behind the Raiffeisen-group in question.

Why do you ask the question open-ended?

It was in the past difficult to bring such issues on the table. Now Raiffeisen goes through a process of renewal. This is a positive thing. The corporate form is just one piece of the Puzzle.

And the new Raiffeisen-President, Guy Lachappelle? He is not burdened by the case of ASE, and the suspicion that the Bank had made too late a money laundering report?

We need to assess whether the leadership of people for a task are appropriate and clean. In our benchmark, if someone had a culpable responsibility. There are also people with experience in large institutions in need. And there's always something wrong. But it can't be that someone for office comes into question, just because he was in the environment of a scandal, for which he bears no personal responsibility. You can't recruit for such a Post, someone from the monastery.

Are you in ten years, Finma's Director, or it pulls you back to a big Bank? There you would also earn more.

I deserve to be here, too good, and by the way, I don't ask myself that question. This is the Job that needs and deserves my hundred percent focus.

(Sunday newspaper)

Created: 13.01.2019, 13:56 PM