Germany: Man armed with machete enters university library and threatens staff

Germany: Man armed with machete enters university library and threatens staff His body naturally produces alcohol, he is acquitted after a drunk driving conviction

His body naturally produces alcohol, he is acquitted after a drunk driving conviction Who is David Pecker, the first key witness in Donald Trump's trial?

Who is David Pecker, the first key witness in Donald Trump's trial? What does the law on the expulsion of migrants to Rwanda adopted by the British Parliament contain?

What does the law on the expulsion of migrants to Rwanda adopted by the British Parliament contain? Spain is the country in the European Union with the most overqualified workers for their jobs

Spain is the country in the European Union with the most overqualified workers for their jobs Parvovirus alert, the “fifth disease” of children which has already caused the death of five babies in 2024

Parvovirus alert, the “fifth disease” of children which has already caused the death of five babies in 2024 Colorectal cancer: what to watch out for in those under 50

Colorectal cancer: what to watch out for in those under 50 H5N1 virus: traces detected in pasteurized milk in the United States

H5N1 virus: traces detected in pasteurized milk in the United States Insurance: SFAM, subsidiary of Indexia, placed in compulsory liquidation

Insurance: SFAM, subsidiary of Indexia, placed in compulsory liquidation Under pressure from Brussels, TikTok deactivates the controversial mechanisms of its TikTok Lite application

Under pressure from Brussels, TikTok deactivates the controversial mechanisms of its TikTok Lite application “I can’t help but panic”: these passengers worried about incidents on Boeing

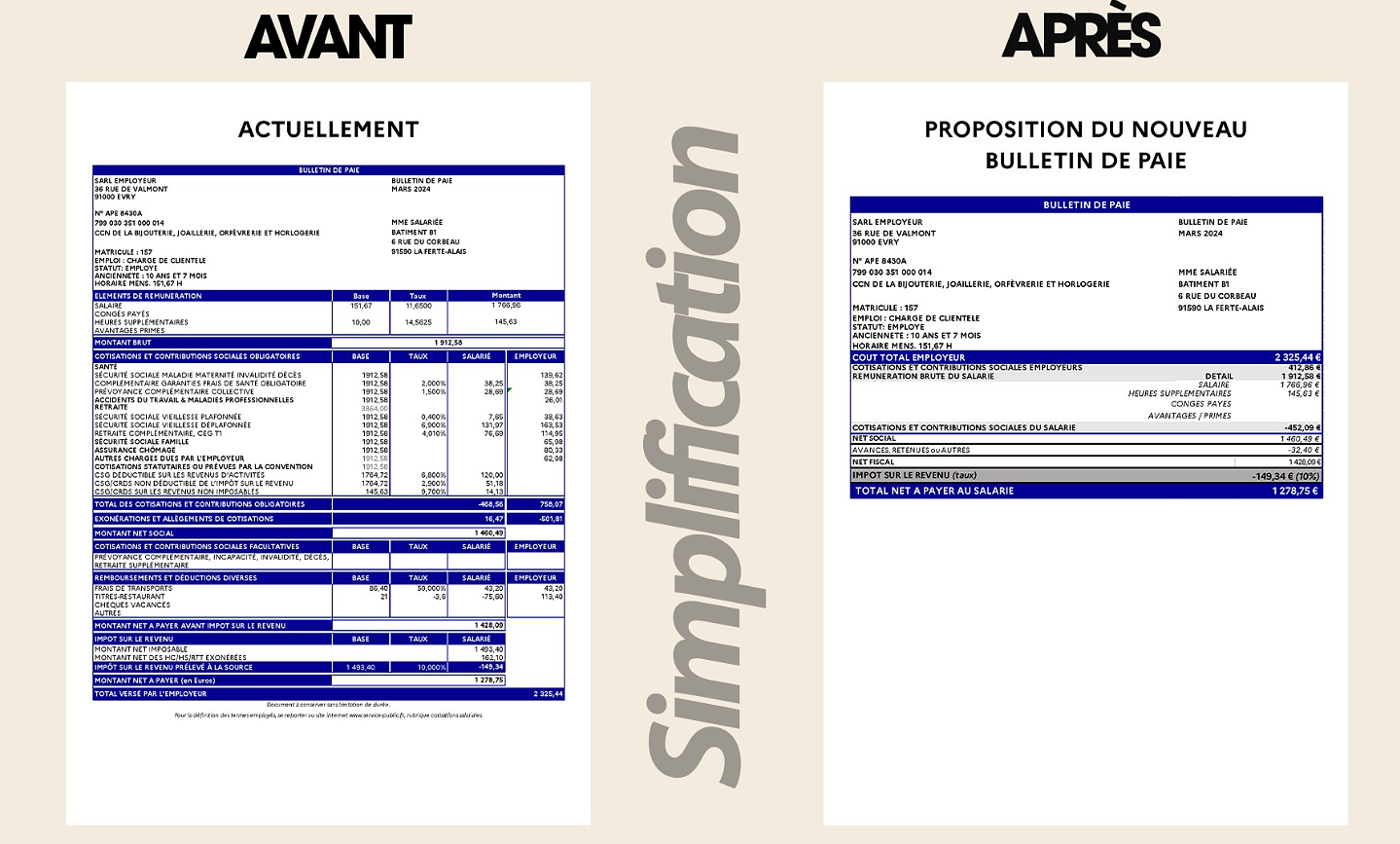

“I can’t help but panic”: these passengers worried about incidents on Boeing “I’m interested in knowing where the money that the State takes from me goes”: Bruno Le Maire’s strange pay slip sparks controversy

“I’m interested in knowing where the money that the State takes from me goes”: Bruno Le Maire’s strange pay slip sparks controversy 25 years later, the actors of Blair Witch Project are still demanding money to match the film's record profits

25 years later, the actors of Blair Witch Project are still demanding money to match the film's record profits At La Scala, Mathilde Charbonneaux is Madame M., Jacqueline Maillan

At La Scala, Mathilde Charbonneaux is Madame M., Jacqueline Maillan Deprived of Hollywood and Western music, Russia gives in to the charms of K-pop and manga

Deprived of Hollywood and Western music, Russia gives in to the charms of K-pop and manga Exhibition: Toni Grand, the incredible odyssey of a sculptural thinker

Exhibition: Toni Grand, the incredible odyssey of a sculptural thinker Skoda Kodiaq 2024: a 'beast' plug-in hybrid SUV

Skoda Kodiaq 2024: a 'beast' plug-in hybrid SUV Tesla launches a new Model Y with 600 km of autonomy at a "more accessible price"

Tesla launches a new Model Y with 600 km of autonomy at a "more accessible price" The 10 best-selling cars in March 2024 in Spain: sales fall due to Easter

The 10 best-selling cars in March 2024 in Spain: sales fall due to Easter A private jet company buys more than 100 flying cars

A private jet company buys more than 100 flying cars This is how housing prices have changed in Spain in the last decade

This is how housing prices have changed in Spain in the last decade The home mortgage firm drops 10% in January and interest soars to 3.46%

The home mortgage firm drops 10% in January and interest soars to 3.46% The jewel of the Rocío de Nagüeles urbanization: a dream villa in Marbella

The jewel of the Rocío de Nagüeles urbanization: a dream villa in Marbella Rental prices grow by 7.3% in February: where does it go up and where does it go down?

Rental prices grow by 7.3% in February: where does it go up and where does it go down? Sale of Biogaran: The Republicans write to Emmanuel Macron

Sale of Biogaran: The Republicans write to Emmanuel Macron Europeans: “All those who claim that we don’t need Europe are liars”, criticizes Bayrou

Europeans: “All those who claim that we don’t need Europe are liars”, criticizes Bayrou With the promise of a “real burst of authority”, Gabriel Attal provokes the ire of the opposition

With the promise of a “real burst of authority”, Gabriel Attal provokes the ire of the opposition Europeans: the schedule of debates to follow between now and June 9

Europeans: the schedule of debates to follow between now and June 9 These French cities that will boycott the World Cup in Qatar

These French cities that will boycott the World Cup in Qatar Hand: Montpellier crushes Kiel and continues to dream of the Champions League

Hand: Montpellier crushes Kiel and continues to dream of the Champions League OM-Nice: a spectacular derby, Niçois timid despite their numerical superiority...The tops and the flops

OM-Nice: a spectacular derby, Niçois timid despite their numerical superiority...The tops and the flops Tennis: 1000 matches and 10 notable encounters by Richard Gasquet

Tennis: 1000 matches and 10 notable encounters by Richard Gasquet Tennis: first victory of the season on clay for Osaka in Madrid

Tennis: first victory of the season on clay for Osaka in Madrid

People want a reliable state pension. But Federal Minister of Finance Christian Lindner wants the "share pension". An equity fund should relieve the pension fund from the middle of the next decade. The federal government wants to make 10 billion available for this in 2023 – partly financed by credit. The whole thing only yields a plus if the income generated exceeds the interest on the loan.

Whether this interest rate bet will ultimately pay off for the state remains to be seen on the financial markets. In any case, a private investor would be advised against financing share purchases with loans. Even more so when hardly anything is known about the planned investment regulations or the risk management of the securities investment.

In order for the calculation to work, the state would have to be willing to gamble on the extremely volatile financial markets in order to achieve the corresponding returns. And in order for the hoped-for lower contributions to be made by the insured, the Minister of Finance would have to continue to feed the capital stock over the next decade.

But despite all the criticism, a good hair can also be found in Lindner's current plan: it is not about the original idea of the FDP "share pension"! Two percent of the pension contribution is not diverted to the capital stock, the pension level is not further reduced and no share-based pension module is created that directly links the amount of the pension payment to the success or failure of the investment policy.

And that's how it should stay. Anyone who transfers capital market risks directly to the pension recipients breaks blatantly with the performance and needs-based principles of the welfare state. The SPD and Minister of Labor Hubertus Heil would do well to continue to oppose the entry of the FDP stock pension into the statutory pension insurance.

The decisive factor will be whether a firewall can be built between the benefits of the pay-as-you-go system and the imponderables of volatile financial markets. If at the end of the day a system should be set up in which the state invests a value-preserving “demographic reserve” to finance higher pension payments in the future and transfers the proceeds to the solidarity system, this could contribute to strengthening the pay-as-you-go system.

This approach would not be entirely new. Social associations and trade unions have repeatedly made proposals to be able to build up more reserves in social security. And in pension insurance, different forms of financial reserve formation were practiced until 1969. The limitation of today's fluctuation reserve (sustainability reserve) to a maximum of 1.5 monthly expenses is relatively recent - and the financial self-restraint is not set in stone.

Those who really want to make the solidarity system fit for the future can build on these traditions. The focus should be on reforms that benefit the insured and not the financial markets. These include a stabilized and gradually increasing pension level, flexible exit options and an employee insurance that everyone pays into.

Instead of an FDP stock pension, the IG Metall proposal for a “Soli-Rente Plus” will also help when it comes to additional provision. With it, more people could already use the options for additional contribution payments that are already available, build up additional entitlements and at the same time strengthen the solidarity system. In this context, it can make sense to create reserves and invest them in a way that preserves their value. The Bundesbank could invest the accumulated contributions according to low-risk criteria and thus tie in with tried-and-tested practice in the German welfare state.

It is crucial that the benefits increased in this way are based on the proven principles of pension insurance and not on the risks of volatile financial markets. Neither contributors nor retirees can afford speculative adventures. When it comes to the statutory pension, you need predictability. In other words: solidarity pension instead of share pension!