Knife attack in Australia: who are the two French heroes congratulated by Macron?

Knife attack in Australia: who are the two French heroes congratulated by Macron? Faced with an anxious Chinese student, Olaf Scholz assures that not everyone smokes cannabis in Germany

Faced with an anxious Chinese student, Olaf Scholz assures that not everyone smokes cannabis in Germany In the Solomon Islands, legislative elections crucial for security in the Pacific

In the Solomon Islands, legislative elections crucial for security in the Pacific Sudan ravaged by a year of war

Sudan ravaged by a year of war Covid-19: everything you need to know about the new vaccination campaign which is starting

Covid-19: everything you need to know about the new vaccination campaign which is starting The best laptops of the moment boast artificial intelligence

The best laptops of the moment boast artificial intelligence Amazon invests 700 million in robotizing its warehouses in Europe

Amazon invests 700 million in robotizing its warehouses in Europe Inflation rises to 3.2% in March due to gasoline and electricity bills

Inflation rises to 3.2% in March due to gasoline and electricity bills Olympic Games-2024: which professions are likely to strike during the competition?

Olympic Games-2024: which professions are likely to strike during the competition? Pizzas sold throughout France recalled for “possible presence” of glass debris

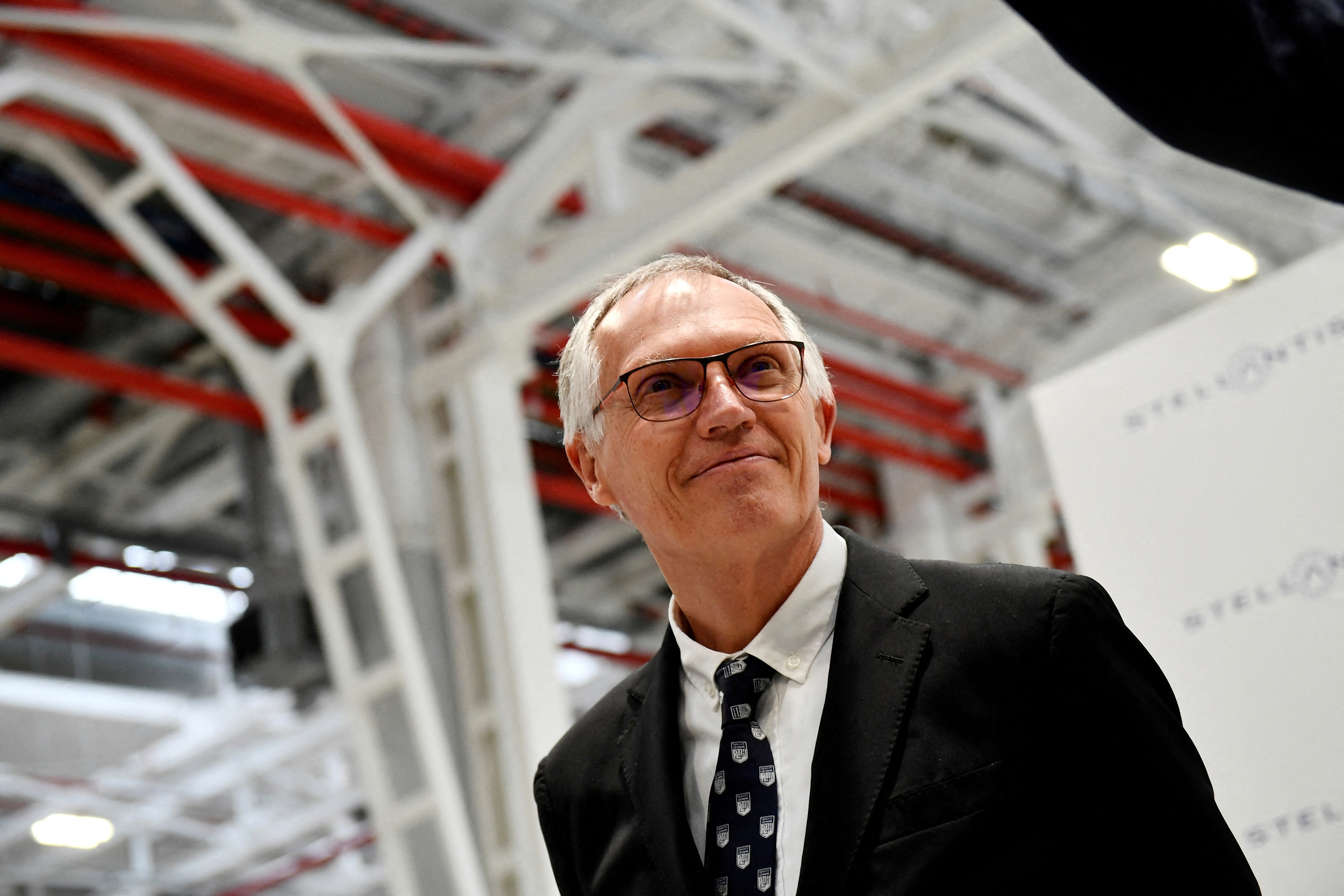

Pizzas sold throughout France recalled for “possible presence” of glass debris “As for a football player, there is a contract”: Carlos Tavares defends his remuneration of 36.5 million euros

“As for a football player, there is a contract”: Carlos Tavares defends his remuneration of 36.5 million euros Stellantis: shareholders validate the controversial remuneration of Carlos Tavares

Stellantis: shareholders validate the controversial remuneration of Carlos Tavares Dune 3 will be the last film of Denis Villeneuve's adaptation

Dune 3 will be the last film of Denis Villeneuve's adaptation Shane Atkinson, humble disciple of the Coen brothers

Shane Atkinson, humble disciple of the Coen brothers Outcry from publishers against the authorization of advertising for books on television

Outcry from publishers against the authorization of advertising for books on television Eddy de Pretto celebrates his “last party too many” at the Olympia

Eddy de Pretto celebrates his “last party too many” at the Olympia Skoda Kodiaq 2024: a 'beast' plug-in hybrid SUV

Skoda Kodiaq 2024: a 'beast' plug-in hybrid SUV Tesla launches a new Model Y with 600 km of autonomy at a "more accessible price"

Tesla launches a new Model Y with 600 km of autonomy at a "more accessible price" The 10 best-selling cars in March 2024 in Spain: sales fall due to Easter

The 10 best-selling cars in March 2024 in Spain: sales fall due to Easter A private jet company buys more than 100 flying cars

A private jet company buys more than 100 flying cars This is how housing prices have changed in Spain in the last decade

This is how housing prices have changed in Spain in the last decade The home mortgage firm drops 10% in January and interest soars to 3.46%

The home mortgage firm drops 10% in January and interest soars to 3.46% The jewel of the Rocío de Nagüeles urbanization: a dream villa in Marbella

The jewel of the Rocío de Nagüeles urbanization: a dream villa in Marbella Rental prices grow by 7.3% in February: where does it go up and where does it go down?

Rental prices grow by 7.3% in February: where does it go up and where does it go down? Europeans: the schedule of debates to follow between now and June 9

Europeans: the schedule of debates to follow between now and June 9 Europeans: “In France, there is a left and there is a right,” assures Bellamy

Europeans: “In France, there is a left and there is a right,” assures Bellamy During the night of the economy, the right points out the budgetary flaws of the macronie

During the night of the economy, the right points out the budgetary flaws of the macronie Europeans: Glucksmann denounces “Emmanuel Macron’s failure” in the face of Bardella’s success

Europeans: Glucksmann denounces “Emmanuel Macron’s failure” in the face of Bardella’s success These French cities that will boycott the World Cup in Qatar

These French cities that will boycott the World Cup in Qatar Dortmund-Atlético: two months before the Euro, Griezmann warms up the engine

Dortmund-Atlético: two months before the Euro, Griezmann warms up the engine Football: Bernd Hölzenbein, 1974 world champion, died at 78

Football: Bernd Hölzenbein, 1974 world champion, died at 78 'Everything comes to an end': Surfing legend Kelly Slater moves closer to retirement

'Everything comes to an end': Surfing legend Kelly Slater moves closer to retirement Athletics: the victory of a transgender athlete causes controversy in the United States

Athletics: the victory of a transgender athlete causes controversy in the United States

2022 has not given any kind of truce to those with mortgages. The 12-month Euribor has risen meteorically each and every month of the year that is ending. This mortgage indicator started the year with the hangover of the historical lows of -0.502% left by December 2021. In April it stopped trading negatively and the ECB's incessant rate hikes did the rest, catapulting its value, especially from July, when the European Central Bank (ECB) applied the first rate hike of the year.

The average data for this last month of the year, which is used to review the price of credits, has risen to 3.018%, after exceeding 3% yesterday, a level not seen since December 2008, when the 3.452% coinciding with the fall of Lehman Brothers that accelerated the monetary stimuli that would lead this indicator to 0%.

Therefore, this year the Euribor has closed with the most abrupt rise since 2000. In the daily rate, the Euribor has climbed today to 3.291%, from 3.285% yesterday.

The four rises in the price of money that the main European monetary institution has undertaken this year have raised interest rates by 250 basis points (from 0% at the beginning of the year to 2.5% today) to try to put stop exorbitant prices in the euro zone, where inflation exceeds 10% and is five times its medium-term objective.

However, in these twelve months the Euribor, which anticipates expectations of further rises (or falls) in official interest rates, has tightened even more and has climbed 350 basis points, due to the aggressiveness of the ECB shown in the face of the future since in the last meeting its president, Christine Lagarde, indicated that "significantly more increases" in rates are still needed and in a sustained manner to control inflation.

As of today, the spread between interest rates and the 12-month interbank rate is 50 basis points.

With these increases, those mortgaged who have to review the bill of their home with the December data, will once again see their quota increased.

With the data for December, 3.018%, in the case of an average mortgage of 150,000 euros at 25 years and a differential of around 1% over the Euribor, those mortgaged will have to pay a total of 793 euros per month, compared to the 532 euros that they disbursed up to now. That is to say, they will have to pay 261 euros more per month or what is the same, 3,132 more per year.

Among the many milestones left by this mortgage index, which affects three out of four mortgagees (some 4.1 million people), it stands out that in September it suffered the highest price increase in history, shooting up 984 thousandths compared to August and 272 basis points. compared to September a year earlier. So it closed that month at 2.233%.

In addition, the Euribor exceeded 3% in its daily rate on December 19 for the first time in 14 years, specifically since January 1, 2009.

The tireless climb of this mortgage indicator does not end here. Experts predict new advances that will go hand in hand with rate hikes that could reach 3.5% during the first half of 2023.

Bankinter sees this indicator in December 2023 at around 4% and is confident that it will drop to 2.2% in 2024. The Fundación de las Cajas de Ahorros (Funcas) indicates that Euribor could be at an average of 3.1% in the middle of 2023, to later decrease slightly.

Fernando López, Chief Operating Officer of gibobs allbanks, admits that it is very likely that for the first quarter of 2023 "interest rates will continue to rise to adjust to the rise in the Euribor announced by the ECB, but in a softer way than what They have been doing it since mid-2022." And Joaquín Robles, from XTB, estimates that the Euribor could be close to 3.5% in the first half of 2023, depending on how inflation and rate forecasts evolve.

These rises in the Euribor have another derivative: mortgage prices will become more tense. So far this year they have already suffered a significant rise, especially fixed loans, but in recent weeks, there has been a lull in the home purchase loan window.

The banking entities have maintained the offers after a strong process of increases in the modality at a fixed rate, and a general improvement in the conditions at a variable rate. However, the rupture of the psychological level of 3% in the Euribor could fuel new rises in mortgages so that banks can defend their margins.

In this scenario, the rates of fixed-rate loans could advance to a band between 4.5% and 5% APR (equivalent annual rate), which includes all expenses.

The Executive reacted to the aggressiveness of the ECB a few weeks ago with a package of measures focused on limiting increases in mortgages and extending their terms for those who have up to 29,400 euros of income.