Germany: Man armed with machete enters university library and threatens staff

Germany: Man armed with machete enters university library and threatens staff His body naturally produces alcohol, he is acquitted after a drunk driving conviction

His body naturally produces alcohol, he is acquitted after a drunk driving conviction Who is David Pecker, the first key witness in Donald Trump's trial?

Who is David Pecker, the first key witness in Donald Trump's trial? What does the law on the expulsion of migrants to Rwanda adopted by the British Parliament contain?

What does the law on the expulsion of migrants to Rwanda adopted by the British Parliament contain? Spain is the country in the European Union with the most overqualified workers for their jobs

Spain is the country in the European Union with the most overqualified workers for their jobs Parvovirus alert, the “fifth disease” of children which has already caused the death of five babies in 2024

Parvovirus alert, the “fifth disease” of children which has already caused the death of five babies in 2024 Colorectal cancer: what to watch out for in those under 50

Colorectal cancer: what to watch out for in those under 50 H5N1 virus: traces detected in pasteurized milk in the United States

H5N1 virus: traces detected in pasteurized milk in the United States Insurance: SFAM, subsidiary of Indexia, placed in compulsory liquidation

Insurance: SFAM, subsidiary of Indexia, placed in compulsory liquidation Under pressure from Brussels, TikTok deactivates the controversial mechanisms of its TikTok Lite application

Under pressure from Brussels, TikTok deactivates the controversial mechanisms of its TikTok Lite application “I can’t help but panic”: these passengers worried about incidents on Boeing

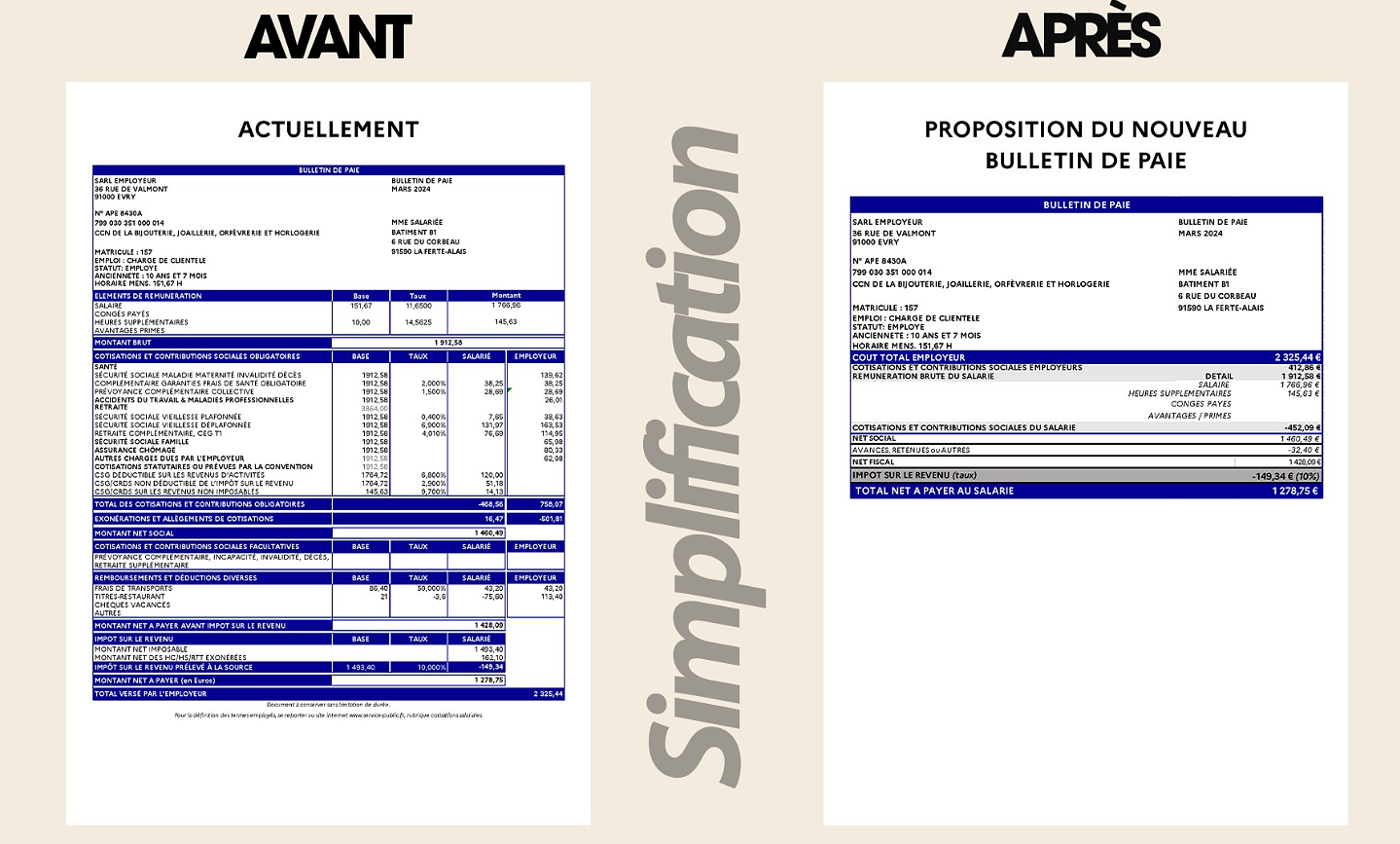

“I can’t help but panic”: these passengers worried about incidents on Boeing “I’m interested in knowing where the money that the State takes from me goes”: Bruno Le Maire’s strange pay slip sparks controversy

“I’m interested in knowing where the money that the State takes from me goes”: Bruno Le Maire’s strange pay slip sparks controversy 25 years later, the actors of Blair Witch Project are still demanding money to match the film's record profits

25 years later, the actors of Blair Witch Project are still demanding money to match the film's record profits At La Scala, Mathilde Charbonneaux is Madame M., Jacqueline Maillan

At La Scala, Mathilde Charbonneaux is Madame M., Jacqueline Maillan Deprived of Hollywood and Western music, Russia gives in to the charms of K-pop and manga

Deprived of Hollywood and Western music, Russia gives in to the charms of K-pop and manga Exhibition: Toni Grand, the incredible odyssey of a sculptural thinker

Exhibition: Toni Grand, the incredible odyssey of a sculptural thinker Skoda Kodiaq 2024: a 'beast' plug-in hybrid SUV

Skoda Kodiaq 2024: a 'beast' plug-in hybrid SUV Tesla launches a new Model Y with 600 km of autonomy at a "more accessible price"

Tesla launches a new Model Y with 600 km of autonomy at a "more accessible price" The 10 best-selling cars in March 2024 in Spain: sales fall due to Easter

The 10 best-selling cars in March 2024 in Spain: sales fall due to Easter A private jet company buys more than 100 flying cars

A private jet company buys more than 100 flying cars This is how housing prices have changed in Spain in the last decade

This is how housing prices have changed in Spain in the last decade The home mortgage firm drops 10% in January and interest soars to 3.46%

The home mortgage firm drops 10% in January and interest soars to 3.46% The jewel of the Rocío de Nagüeles urbanization: a dream villa in Marbella

The jewel of the Rocío de Nagüeles urbanization: a dream villa in Marbella Rental prices grow by 7.3% in February: where does it go up and where does it go down?

Rental prices grow by 7.3% in February: where does it go up and where does it go down? Sale of Biogaran: The Republicans write to Emmanuel Macron

Sale of Biogaran: The Republicans write to Emmanuel Macron Europeans: “All those who claim that we don’t need Europe are liars”, criticizes Bayrou

Europeans: “All those who claim that we don’t need Europe are liars”, criticizes Bayrou With the promise of a “real burst of authority”, Gabriel Attal provokes the ire of the opposition

With the promise of a “real burst of authority”, Gabriel Attal provokes the ire of the opposition Europeans: the schedule of debates to follow between now and June 9

Europeans: the schedule of debates to follow between now and June 9 These French cities that will boycott the World Cup in Qatar

These French cities that will boycott the World Cup in Qatar Hand: Montpellier crushes Kiel and continues to dream of the Champions League

Hand: Montpellier crushes Kiel and continues to dream of the Champions League OM-Nice: a spectacular derby, Niçois timid despite their numerical superiority...The tops and the flops

OM-Nice: a spectacular derby, Niçois timid despite their numerical superiority...The tops and the flops Tennis: 1000 matches and 10 notable encounters by Richard Gasquet

Tennis: 1000 matches and 10 notable encounters by Richard Gasquet Tennis: first victory of the season on clay for Osaka in Madrid

Tennis: first victory of the season on clay for Osaka in Madrid

The value of tomorrow is produced in partnership with Zonebourse.com

When we talk about the pharmaceutical industry, we think of Roche, Sanofi, Teva or more recently Moderna. But these laboratories rely on a network of third-party companies for a certain number of operations that they cannot or do not want to carry out internally. Valais Lonza is one of them. It is even the main manufacturer of the pharmaceutical world. Toll manufacturing is producing to order for someone else. The term is more elegant than its Anglo-Saxon equivalent, CDMO, literally "contract development and manufacturing organization".

For years, Lonza kept a foothold in specialty chemicals, before choosing to focus on the most lucrative part of the industry, healthcare. The group is now divided into four complementary entities: biological products (50% of revenues), small molecules (14%), cell and gene therapies (11%) and finally capsules and health ingredients (22%). The gross operating surplus margin (Ebitda) is between 30 and 40% for all divisions, except for cell and gene therapies, which fluctuate between 15 and 20%. Just over 60% of revenues are generated by large global laboratories, which gives the group a comfortable footing. The geographical distribution of activity is fairly balanced between North America (47%) and Europe (40%), the balance coming from Asia Pacific (13%).

Lonza operates in a sector with high barriers to entry. The healthcare industry is subject to extremely strict rules with high standards. The contractors must be both innovative and rigorous in their management because the start-up of projects is costly. What's more, the relationship of trust and know-how are considerable, if not essential, assets. If we put all this end to end, it is easy to understand that the economic model allows significant margins and that there is a considerable premium in favor of the players in place. This explains why Lonza is everywhere, with more than a thousand projects in progress, from the most classic to the most complex. It is, for example, the subcontractor who had been chosen by Moderna to urgently produce the active ingredient of the vaccine against Covid-19, with unprecedented volume challenges.

At the economic level, Lonza has thus become a one-stop shop for the biotechnology and pharmaceutical industry, to steal the formula from a good connoisseur of the sector. In the stock market, it is a means of investing on the theme of biotechnology without bearing the binary risk generally associated with clinical development. Its current capitalization of 35 billion Swiss francs makes it one of the ten largest companies in the Confederation, for a turnover which should exceed 6.2 billion Swiss francs this year. As for margins, they are high and constantly increasing, especially since its more traditional chemicals activities were sold to the Cinven and Bain Capital funds in 2021. An operation which moreover completely erased the debt.

Leader in a health sector with high barriers to entry, well diversified, essential and present on underlying trends... Any somewhat enlightened investor expects a hefty bill. No miracle, it is the case: at more than 30 times the results expected this year, the Swiss company is at the top of the sector basket. However, it is quite a unique asset and its growth trajectory is solid. What's more, the stock has lost 40% since the start of the year, which has erased the excesses of the second half of 2021. This is a credible candidate for those looking for a long-term position with robust fundamentals. .