Germany: Man armed with machete enters university library and threatens staff

Germany: Man armed with machete enters university library and threatens staff His body naturally produces alcohol, he is acquitted after a drunk driving conviction

His body naturally produces alcohol, he is acquitted after a drunk driving conviction Who is David Pecker, the first key witness in Donald Trump's trial?

Who is David Pecker, the first key witness in Donald Trump's trial? What does the law on the expulsion of migrants to Rwanda adopted by the British Parliament contain?

What does the law on the expulsion of migrants to Rwanda adopted by the British Parliament contain? Spain is the country in the European Union with the most overqualified workers for their jobs

Spain is the country in the European Union with the most overqualified workers for their jobs Parvovirus alert, the “fifth disease” of children which has already caused the death of five babies in 2024

Parvovirus alert, the “fifth disease” of children which has already caused the death of five babies in 2024 Colorectal cancer: what to watch out for in those under 50

Colorectal cancer: what to watch out for in those under 50 H5N1 virus: traces detected in pasteurized milk in the United States

H5N1 virus: traces detected in pasteurized milk in the United States Insurance: SFAM, subsidiary of Indexia, placed in compulsory liquidation

Insurance: SFAM, subsidiary of Indexia, placed in compulsory liquidation Under pressure from Brussels, TikTok deactivates the controversial mechanisms of its TikTok Lite application

Under pressure from Brussels, TikTok deactivates the controversial mechanisms of its TikTok Lite application “I can’t help but panic”: these passengers worried about incidents on Boeing

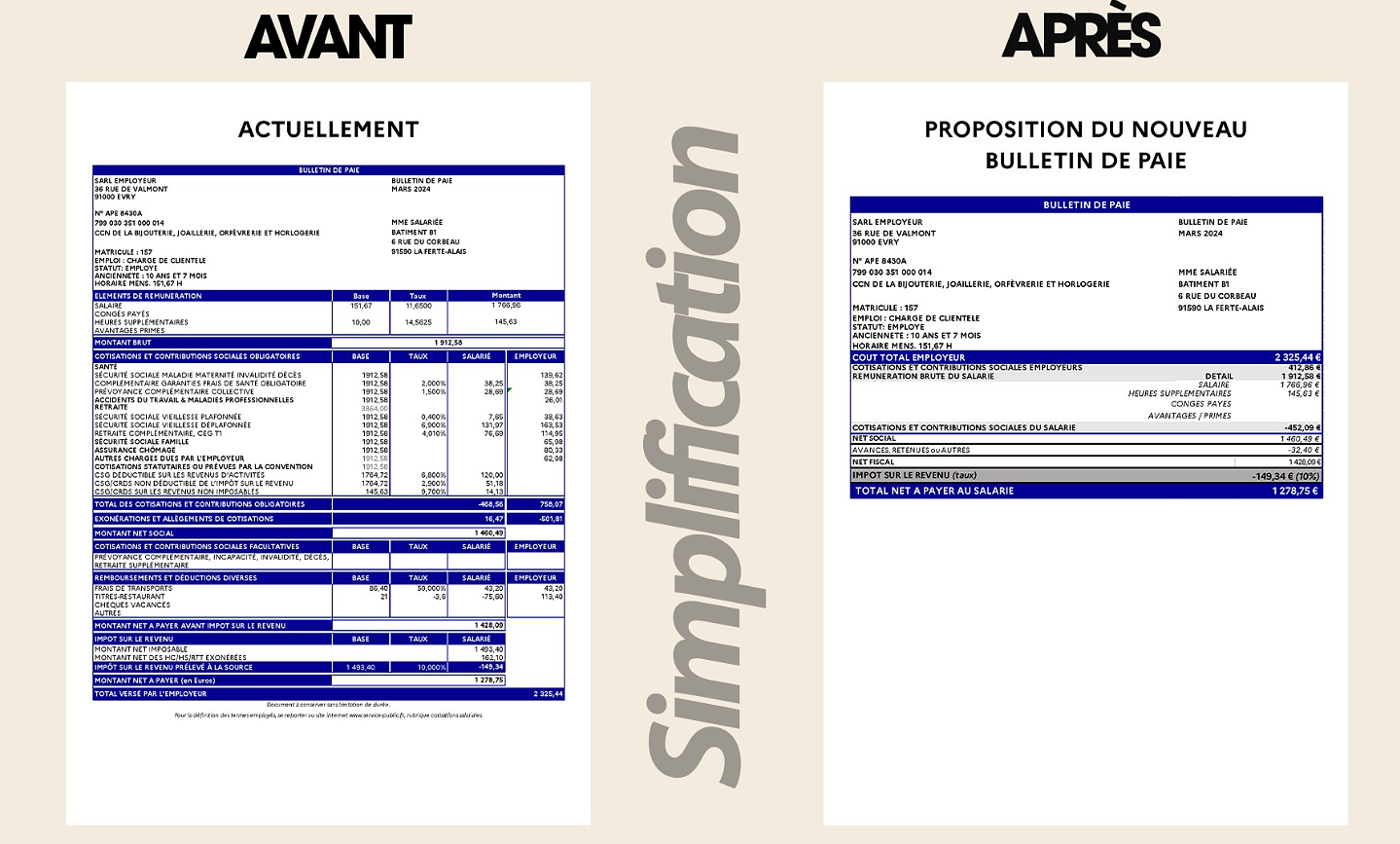

“I can’t help but panic”: these passengers worried about incidents on Boeing “I’m interested in knowing where the money that the State takes from me goes”: Bruno Le Maire’s strange pay slip sparks controversy

“I’m interested in knowing where the money that the State takes from me goes”: Bruno Le Maire’s strange pay slip sparks controversy 25 years later, the actors of Blair Witch Project are still demanding money to match the film's record profits

25 years later, the actors of Blair Witch Project are still demanding money to match the film's record profits At La Scala, Mathilde Charbonneaux is Madame M., Jacqueline Maillan

At La Scala, Mathilde Charbonneaux is Madame M., Jacqueline Maillan Deprived of Hollywood and Western music, Russia gives in to the charms of K-pop and manga

Deprived of Hollywood and Western music, Russia gives in to the charms of K-pop and manga Exhibition: Toni Grand, the incredible odyssey of a sculptural thinker

Exhibition: Toni Grand, the incredible odyssey of a sculptural thinker Skoda Kodiaq 2024: a 'beast' plug-in hybrid SUV

Skoda Kodiaq 2024: a 'beast' plug-in hybrid SUV Tesla launches a new Model Y with 600 km of autonomy at a "more accessible price"

Tesla launches a new Model Y with 600 km of autonomy at a "more accessible price" The 10 best-selling cars in March 2024 in Spain: sales fall due to Easter

The 10 best-selling cars in March 2024 in Spain: sales fall due to Easter A private jet company buys more than 100 flying cars

A private jet company buys more than 100 flying cars This is how housing prices have changed in Spain in the last decade

This is how housing prices have changed in Spain in the last decade The home mortgage firm drops 10% in January and interest soars to 3.46%

The home mortgage firm drops 10% in January and interest soars to 3.46% The jewel of the Rocío de Nagüeles urbanization: a dream villa in Marbella

The jewel of the Rocío de Nagüeles urbanization: a dream villa in Marbella Rental prices grow by 7.3% in February: where does it go up and where does it go down?

Rental prices grow by 7.3% in February: where does it go up and where does it go down? Sale of Biogaran: The Republicans write to Emmanuel Macron

Sale of Biogaran: The Republicans write to Emmanuel Macron Europeans: “All those who claim that we don’t need Europe are liars”, criticizes Bayrou

Europeans: “All those who claim that we don’t need Europe are liars”, criticizes Bayrou With the promise of a “real burst of authority”, Gabriel Attal provokes the ire of the opposition

With the promise of a “real burst of authority”, Gabriel Attal provokes the ire of the opposition Europeans: the schedule of debates to follow between now and June 9

Europeans: the schedule of debates to follow between now and June 9 These French cities that will boycott the World Cup in Qatar

These French cities that will boycott the World Cup in Qatar Hand: Montpellier crushes Kiel and continues to dream of the Champions League

Hand: Montpellier crushes Kiel and continues to dream of the Champions League OM-Nice: a spectacular derby, Niçois timid despite their numerical superiority...The tops and the flops

OM-Nice: a spectacular derby, Niçois timid despite their numerical superiority...The tops and the flops Tennis: 1000 matches and 10 notable encounters by Richard Gasquet

Tennis: 1000 matches and 10 notable encounters by Richard Gasquet Tennis: first victory of the season on clay for Osaka in Madrid

Tennis: first victory of the season on clay for Osaka in Madrid

In the occupational Pension plans have been active in the past ten years, funds in the order of over 90 billion Swiss francs of the purchase to be redistributed to the Retired. The data, collected by the pension consultant PPC Metrics for the Sunday newspaper.

This sum is far higher than previously assumed. So far, only those Numbers were known, which raises the Occupational Pension Supervisory Commission for five years. After that, between 2014 and 2018, have been redistributed to around 33.5 billion francs, as it announced on Tuesday. This corresponds to, on average, 6.7 billion per year.

The Figures for earlier years show that the redistribution from 2009 to 2013 was even higher. She moved in the order of 12 billion Swiss francs per year. This also has to do with the pension funds after the financial crisis, its income had to fill the reserve pots, before they could credit the capital in the workforce again earned.

Until retirement, the bill will be presented

The redistribution was, however, already prior to 2009. According to a report by the oversight Commission, on actions already from 1997 onwards, the gaps in the financing of the pensions. The yields of the pension funds were even then not in every year, high enough to Finance the pensions. After the good stock market years of the nineties, the funds had accumulated their reserves, however, and were able to close the gaps. At the latest after 2007, the yields and the promised pensions gaped wide apart, and the reserves were exhausted. Thus, the acquisition had to inanzieren make with their accumulated capital with the pension claims.

The acquisition not to make yourself know how much of your money was redistributed. It is only when you retire, you get presented with the bill: to calculate your pension from the occupational Pension, is multiplied by your retirement capital using the conversion rate and both of these factors are currently low. The capital employed has only grown slowly, because it was remunerated on the basis of redistribution is often lower than that of the pensioners. In addition, many pension funds have lowered the conversion rate according to pension consultant Complementa to an average of 5.6 percent in the current year. And you will sink up to 2024, further, to 5.3 percent.

For the employed, it makes a big difference, whether you go with a conversion rate of 6.8 or 5.6 percent in retirement, and how big your capital is. Who could save 500'000 Swiss francs with a conversion rate of 6.8 percent in retirement was adopted, receives a monthly pension of 2833 Swiss francs from the second pillar. The one who comes due to the redistribution of only 400'000 Swiss francs and whose pension was calculated using a conversion rate of 5.6 percent, receives only in 1866, franc – scarce 1000 francs less.

Insured persons in the supplementary benefits

driven This 1000 francs difference can decide whether someone on supplementary benefits will be dependent or not The pension is not huge. It is for individuals between 1185 and 2370 Swiss francs.

Suppose that someone receives from the first column the average of these two Numbers, 1777 francs, and from the second pillar, the 1866 francs, the pension 3644 Swiss francs. To come up with such an income to make ends meet, is not only in cities a challenge.

"The pension funds today are able to generate the returns it needs to pay the promised pension, with a high investment risk," says Marco Jost, a pension Fund expert of PPC Metrics. And many do, as is clear from the collection of the supervision Commission. 53 percent to follow an investment strategy with a rather high or high risk. If this strategy doesn't work out, pay alone working for it. You will receive less interest or even help to refurbish your office.

investors must be happy, if you do not have to pay negative interest rates.

However, those funds that insure only the legally required minimum pension are forced, a conversion rate of 6.8 percent to apply. The Problem is, that the legislature went out in the eighties, the funds can always earn a safe yield of at least 4 percent. He has set the conversion rate accordingly. Today, however, without risk, no return and more safely achieve. Investors must already be glad, if you do not have to pay negative interest rates.

daure the longer The phase of low interest rates now, however, the bigger the mountain of debt or the obligations, which the pension funds are entered into with the guaranteed pensions, will Marco Jost says. Therefore, you should discuss honestly about how it can be remove again.

However, There were also years in which, in the other direction was redistributed to the pensioners to the employed. This was in the nineties, when the interest rate level was significantly higher than the conversion rate. The pension funds did not know at the time, almost, where with the money and granted to the employed, among other things, "contribution holiday".

This Text is from the current issue. Now all of the articles in the E-Paper of the Sunday newspaper, read: App for iOS App for Android – Web-App (Sunday newspaper)

Created: 19.05.2019, 00:23 PM