His body naturally produces alcohol, he is acquitted after a drunk driving conviction

His body naturally produces alcohol, he is acquitted after a drunk driving conviction Who is David Pecker, the first key witness in Donald Trump's trial?

Who is David Pecker, the first key witness in Donald Trump's trial? What does the law on the expulsion of migrants to Rwanda adopted by the British Parliament contain?

What does the law on the expulsion of migrants to Rwanda adopted by the British Parliament contain? The shadow of Chinese espionage hangs over Westminster

The shadow of Chinese espionage hangs over Westminster Parvovirus alert, the “fifth disease” of children which has already caused the death of five babies in 2024

Parvovirus alert, the “fifth disease” of children which has already caused the death of five babies in 2024 Colorectal cancer: what to watch out for in those under 50

Colorectal cancer: what to watch out for in those under 50 H5N1 virus: traces detected in pasteurized milk in the United States

H5N1 virus: traces detected in pasteurized milk in the United States What High Blood Pressure Does to Your Body (And Why It Should Be Treated)

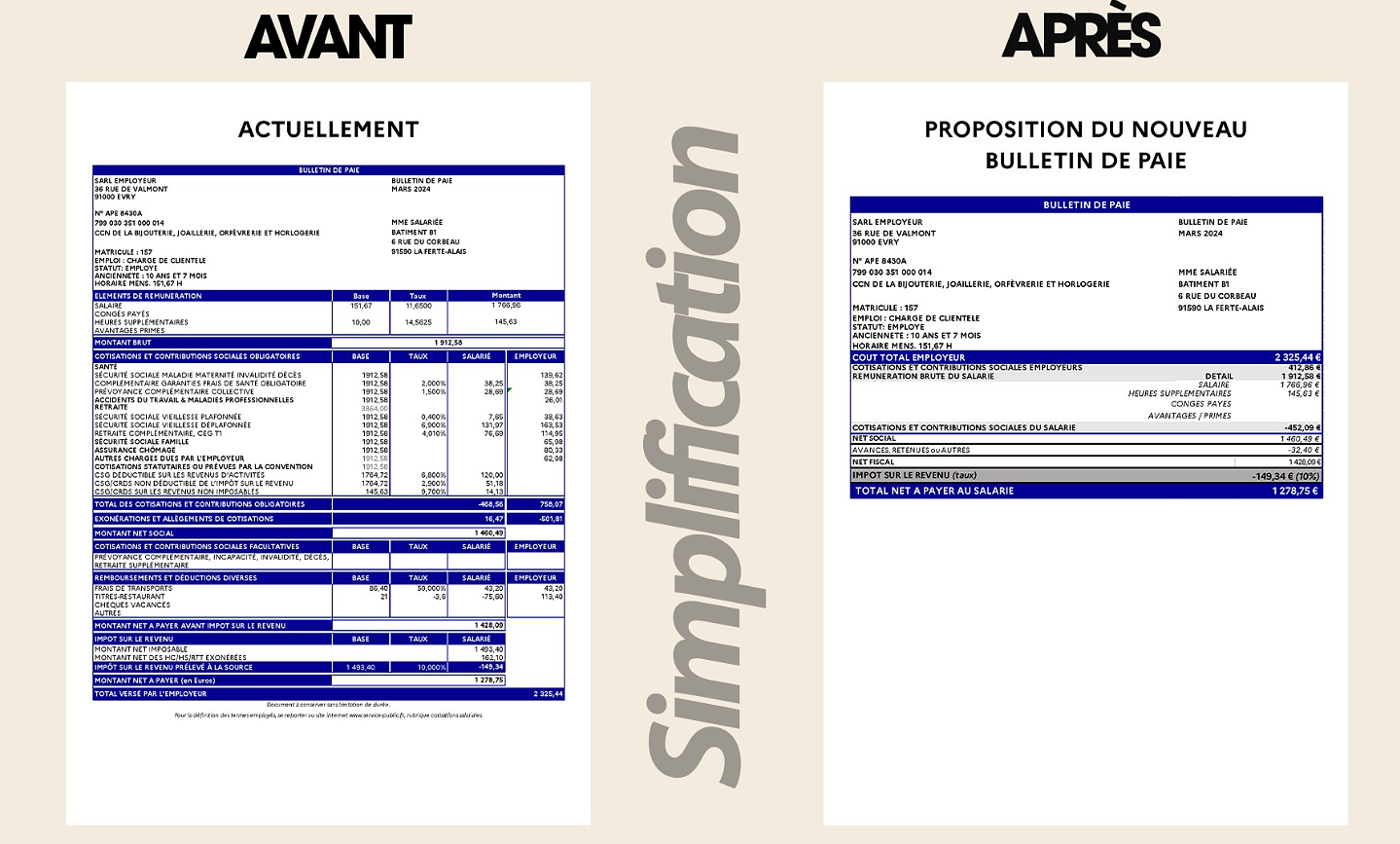

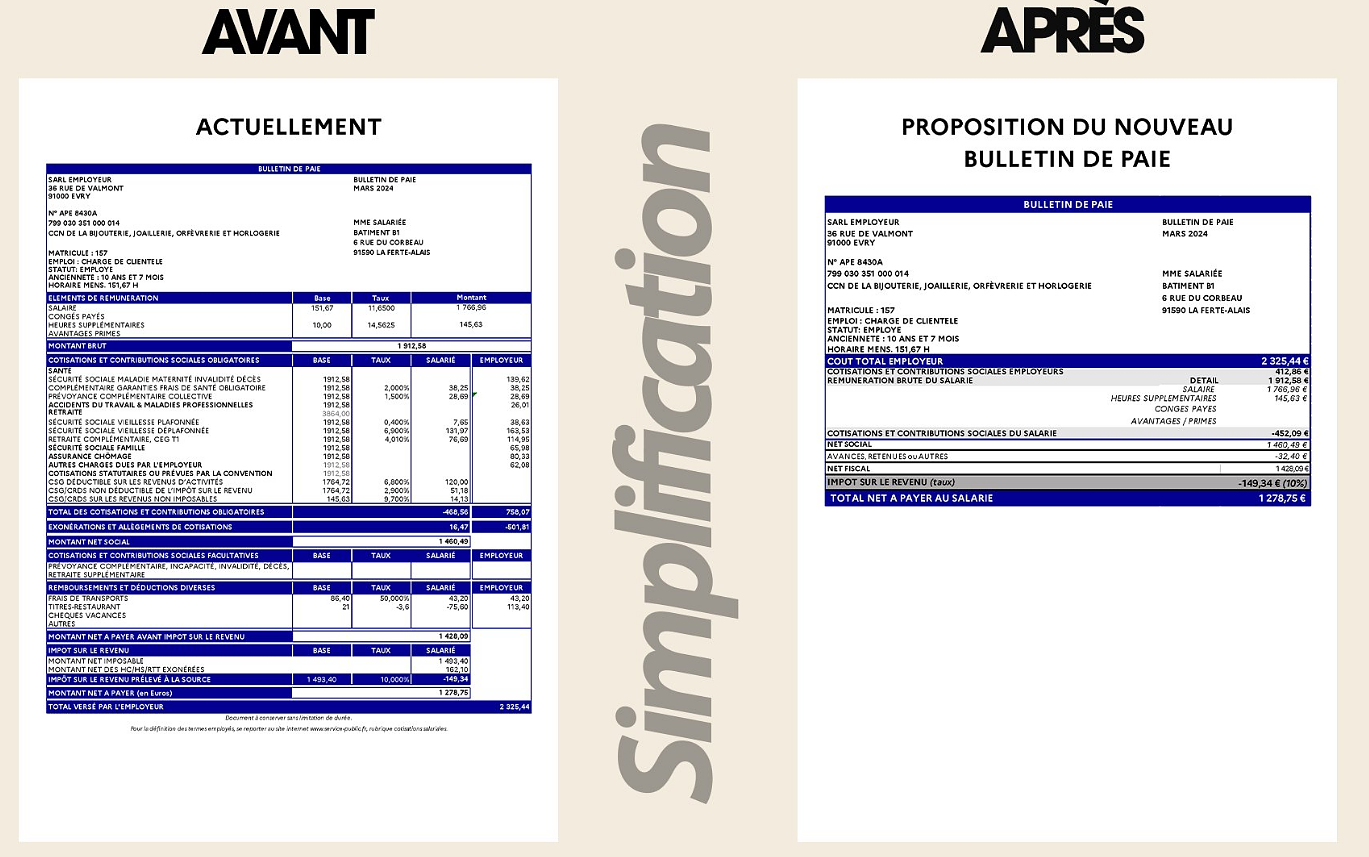

What High Blood Pressure Does to Your Body (And Why It Should Be Treated) “I’m interested in knowing where the money that the State takes from me goes”: Bruno Le Maire’s strange pay slip sparks controversy

“I’m interested in knowing where the money that the State takes from me goes”: Bruno Le Maire’s strange pay slip sparks controversy Despite the lifting of the controllers' strike, massive flight cancellations planned for Thursday, April 25

Despite the lifting of the controllers' strike, massive flight cancellations planned for Thursday, April 25 The right deplores a “dismal agreement” on the end of careers at the SNCF

The right deplores a “dismal agreement” on the end of careers at the SNCF The United States pushes TikTok towards the exit

The United States pushes TikTok towards the exit Saturday is independent bookstore celebration

Saturday is independent bookstore celebration In Paris as in Marseille, the Flames ceremony opens to fans of rap and hip-hop

In Paris as in Marseille, the Flames ceremony opens to fans of rap and hip-hop Sale of the century for a mysterious painting by Klimt, in Austria

Sale of the century for a mysterious painting by Klimt, in Austria Philippe Laudenbach, actor with more than a hundred supporting roles, died at 88

Philippe Laudenbach, actor with more than a hundred supporting roles, died at 88 Skoda Kodiaq 2024: a 'beast' plug-in hybrid SUV

Skoda Kodiaq 2024: a 'beast' plug-in hybrid SUV Tesla launches a new Model Y with 600 km of autonomy at a "more accessible price"

Tesla launches a new Model Y with 600 km of autonomy at a "more accessible price" The 10 best-selling cars in March 2024 in Spain: sales fall due to Easter

The 10 best-selling cars in March 2024 in Spain: sales fall due to Easter A private jet company buys more than 100 flying cars

A private jet company buys more than 100 flying cars This is how housing prices have changed in Spain in the last decade

This is how housing prices have changed in Spain in the last decade The home mortgage firm drops 10% in January and interest soars to 3.46%

The home mortgage firm drops 10% in January and interest soars to 3.46% The jewel of the Rocío de Nagüeles urbanization: a dream villa in Marbella

The jewel of the Rocío de Nagüeles urbanization: a dream villa in Marbella Rental prices grow by 7.3% in February: where does it go up and where does it go down?

Rental prices grow by 7.3% in February: where does it go up and where does it go down? Sale of Biogaran: The Republicans write to Emmanuel Macron

Sale of Biogaran: The Republicans write to Emmanuel Macron Europeans: “All those who claim that we don’t need Europe are liars”, criticizes Bayrou

Europeans: “All those who claim that we don’t need Europe are liars”, criticizes Bayrou With the promise of a “real burst of authority”, Gabriel Attal provokes the ire of the opposition

With the promise of a “real burst of authority”, Gabriel Attal provokes the ire of the opposition Europeans: the schedule of debates to follow between now and June 9

Europeans: the schedule of debates to follow between now and June 9 These French cities that will boycott the World Cup in Qatar

These French cities that will boycott the World Cup in Qatar Montpellier-Nantes: at what time and on which channel to watch the Ligue 1 match?

Montpellier-Nantes: at what time and on which channel to watch the Ligue 1 match? Ligue 1: Luis Enrique leaves many PSG players to rest in Lorient

Ligue 1: Luis Enrique leaves many PSG players to rest in Lorient Football: Deschamps, Drogba, Desailly... Beautiful people with Emmanuel Macron to play with the Variétés

Football: Deschamps, Drogba, Desailly... Beautiful people with Emmanuel Macron to play with the Variétés Football: “the referee was bought”, Guy Roux’s anecdote about a European Cup match… with watches and rubies

Football: “the referee was bought”, Guy Roux’s anecdote about a European Cup match… with watches and rubies

time is of The essence. In the case of investment properties, the mortgage market is running hot. For months, the Swiss national Bank warns of the risks that may arise from it. The financial market Supervisory authority (Finma) and the Treasury Department expect to in August, a statement from the banks. Until then, they need to set stricter rules in the mortgage business. This is not done, is take the Federal measures.

to prevent this, the industry is working under high pressure, proposals for a more stringent self-regulation. About the bankers Association of the negotiations, such as the common solution could look like is currently underway. A few days ago, the "Aargauer Zeitung" also helped first vertices. According to the report, real property may be less invested is high with mortgage . The maximum mortgage debt to decline in relation to the property value from 80 to 75 percent. In addition, the mortgage must be paid off faster. The banks of the supervision would meet.

"Internal opinion-forming in the hallway"

A spokeswoman for the bankers Association confirmed that during the discussions, the instruments "payback period" and "loan-to-value ratio" will be discussed in Detail. The values are not confirmed but. Because even within the industry, they are not a long time fix. "In Parallel to the ongoing negotiations with the authorities, our internal opinion formation is still in progress," confirms the spokesperson. However, the bankers Association, assume, to arrive in spite of the possible nuances in the assessment of the situation a clear decision. The opinions are, but: "I hope we can agree, because there is not much time," says an Insider. In the case of the common requirements not only all the banks have to follow suit, the Finma must agree.

Particularly the cantonal banks were reluctant to date against the uniform guidelines. They have settled in the last few years in the mortgage market, the big banks have lost market shares. If the first proposals are in the sense of the cantonal banks, however, remains open. "We don't," said a spokesman for the Association of Swiss cantonal banks to comment on the Figures. The cantonal banks would bring on the bankers Association and the solution also support it. "But we are still skeptical as to whether a comprehensive regulation is the most efficient solution for the Problem in the case of investment properties," said the spokesman. The Association believes that targeted institution-specific measures of supervision for individual banks to make more sense.

"The effect of such measures is backward-looking, corrective and not preventive."Finma chief Mark Branson

The Finma to intervene only in the case of the banks to high risks. The supervision already. And The effect of such measures was backward-looking, corrective and not preventive, so the Finma chief Mark Branson. To have you next an outlier in the handle and dive soon. The approach is not worth more therefore. Since recently, the 18 banks conducted stress test, it is clear that several banks could get into trouble. With the big banks, sees itself as well equipped and would, therefore, have no Problem with that, if the results of the stress would be released tests. Therefore, little understanding for the reluctance of the cantonal banks is there to be felt.

Problem not solved, only

moved if it is not possible for the banks to agree on a compromise, the Finma is already possible measures in the quiver. "The Alternative would be a tightening of capital regulation with a view on the Capital adequacy of investment properties," said a spokesman. Then loans for investment properties, which are invested with more than two-thirds of the market value would have to be stronger with capital. This would also take account of the fact that residential investment property to owner-occupied properties at an increased risk.

the Problem is not likely to be the for the cantonal banks, though. They are very well capitalised, the business is going well. You it is likely to fall slightly, the investment properties with more capital to hedge. Thus, the Problem of rising risks would not be solved in the mortgage market, but simply moved. To avert the risk of a sharp price correction, it needs according to insiders, a Change on the demand side, i.e. in the case of the investors in real estate projects. As long as they are desperately seeking for a little return, and it will change to nothing except the supposed safe rate of return is the property for you unattractive. (Editorial Tamedia)

Created: 17.05.2019, 20:35 PM